Finding ways to reduce financial stress can be overwhelming.

For many people, the figures themselves are difficult to grasp — but they know it means they have to tighten their belts.

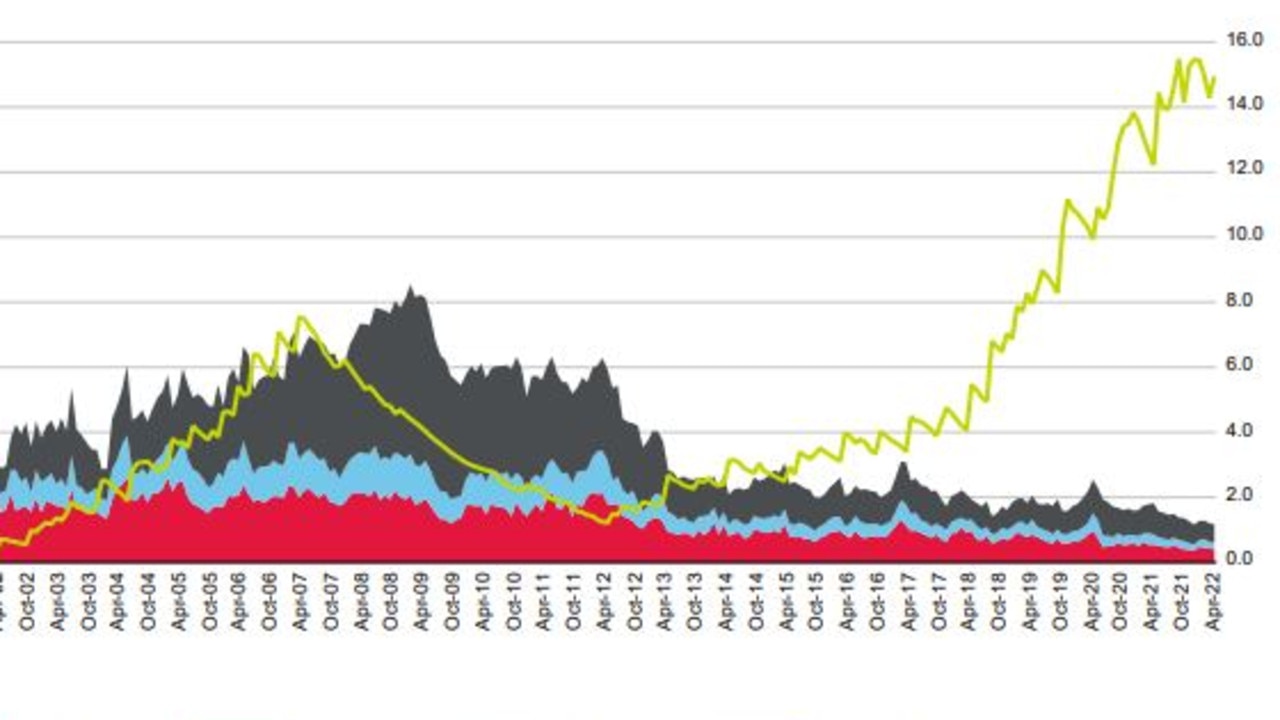

The Reserve Bank of Australia this week increased the cash rate target by 50 basis points to 1.85 per cent.

Annual CPI inflation also increased to 6.1 per cent in the June quarter, due to higher dwelling construction costs and automotive fuel prices.

So what can you do to relieve your financial pressure?

Curtin Business School instructor and financial planner Elson Goh told NCA NewsWire there were four key ways people could save money.

REFINANCING YOUR LOANS

Mr Goh said everyone with a loan should first contact their current lender to try to get a better deal.

“It is often more costly for a lender to acquire a new customer than to retain an existing one,” he said.

“Go into a bank branch and introduce yourself to the lending manager. It can be easier than dealing with a call center representative.”

Mr Goh also recommends people use a mortgage broker.

“A good broker will negotiate a better deal with your current lender and present other suitable opportunities,” he said.

“Your current lender may respond more favorably if your case is presented well.

“For example, it is pointless to be asking your lender to match the rate that your colleague at work was talking about when their loan size is $800,000 while yours is only $350,000.

“You need the right information such as estimated value of your property and whether or not you have 20, 30 or 40 per cent equity in your home.”

Comparison websites can be a useful tool but Mr Goh warns they are not perfect.

“You have to be cautious as some products may be heavily promoted on these sites and not every lender is represented,” he said.

“Additionally, you cannot focus on just the interest rate or the comparison rate, as there are other things like fees, loan features, loan term and product flexibility that must be considered.

“If you are refinancing your home loan, be mindful of the remaining term of your loan.

“If you have had the property and loan for say five years, and you take up a new loan for over 30 years again, you may be delighted that the monthly repayments are much lower and seemingly more affordable.

“But if you only pay the minimum repayments, you may end up paying more interest over the entire duration and take longer to be mortgage free.”

SWITCHING YOUR SUPERANNUATION

The main types of super funds are employer, retail, industry and self-managed.

Mr Goh said before making a switch you should seek advice if you have a defined benefit scheme, constitutionally protected fund, or benefits paid by the employer.

“You will not be able to restore your entitlements once you switch out to another fund,” he said.

“This can also apply to any insurance policies that you currently have in force within your existing fund.

The tax office website is a good place to start your research.

“However, it is futile to chase after returns as past performance is not a good indicator of future outcomes,” Mr Goh said.

“What you should consider is to ensure that you are paying for services and features that you need and check if the fund is investing at a risk level that you are comfortable with.”

INSURANCE AND UTILITIES

Insurance includes personal, home and content, motor vehicle and health, among others

Mr Goh recommends people seek advice when dealing with personal insurance.

“Your health condition was accepted by the insurance company at the time of application,” he said.

“You are covered under the terms of the agreement as long as you pay your premiums, regardless of the changes to your health.

“Any alterations of your personal insurance may result in reassessment of your current health conditions, which may attract a loading of premiums, exclusion of benefits or outright decline of cover.”

General insurance is different and a cheaper policy is often a result of having less coverage or stricter definition for payout.

But Mr Goh said there were things to consider to ensure you pay for what you need.

“For example, your home insurance cover should only be the amount needed to rebuild your house, not the full purchase price,” he said.

“The excess that you pay upon making a claim is a form of self-insurance.

“Your premiums will become cheaper as you increase the excess on your policy. You can increase the excess if you have available funds saved up and have a low claims history.”

FOOD, GOING OUT AND SUBSCRIPTIONS

When it comes to everyday costs like food and going out, Mr Goh recommends people involve the whole family.

“Rather than trying to formulate a battle plan on your own, you may be surprised by the variety of suggestions that would arise from people with different perspectives,” he said.

Mr Goh said people should make small changes over long periods of time, rather than drastic abstinence.

“It is easier to make small manageable changes than large ones that increase your stress levels. The latter often results in increased spending through retail therapy,” he said.

“Get creative and be flexible with your meals. Substitute ingredients that have gone up in price with more affordable alternatives when cooking.

“Or try preserving vegetables and making jams with produce that are in season or abundance.

“These are some of the things that our grandparents did after the war and they managed to thrive despite experiencing similar if not worse inflationary conditions.”

Mr Goh also recommends people look into their monthly subscriptions.

“They are often payments that get overlooked. If you are not fully utilizing the service or subscription, cancel them,” he said.

He also suggests people find ways to reuse and recycle where possible.

“You can breathe new life into old furniture with a new coat of paint or a box of screws,” he said.

.