In the history of Australia, the nation’s economy has often been defined by booms and busts. From the 1890s depression driven by a collapse in wool prices and housing price crash, all the way through to the current boom in thermal coal prices, Australia’s economy has thrived and dived on boom and bust cycles.

In October 2019, the Reserve Bank warned of yet another boom that would turn to a bust, this time in the construction sector. At the time RBA Deputy Governor Guy Debelle made a speech to warn of falling activity in the industry, stating that it would subtract around 1 percentage point from GDP growth and that there was some risk the decline could be even larger.

Around that time investment bank UBS was equally concerned, warning that construction job ads were pointing to around 100,000 jobs potentially being lost in the industry as activity levels dropped from its peak.

With every boom comes a bust

Looking at the data, it’s clear why Debelle and the RBA were concerned about the direction of the industry. Between April 2012 and November 2017, the construction sector underwent an enormous boom following a period of rapidly falling activity resulting from the end of projects driven by the Rudd and Gillard government’s first homeowner grants. During this period dwelling approvals rose by 119 per cent and the construction sector enjoyed a period of strong growth even while other parts of the economy struggled.

But the continued strength of the construction sector was not to be.

Between November 2017 and the pre-pandemic lows of January 2020, dwelling approvals fell by 41.5 per cent. Naturally in time, dwelling commencements also fell from their peaks, dropping by 31.8 per cent between March 2018 and September 2019.

The pandemic effect

At the start of 2020, it was all very much looking like the RBA’s concerns about the future of the construction sector were justified. But when the pandemic arrived on Australia’s shores just a few months later everything changed.

In just a few months the fortunes of the construction sector changed dramatically, from a slowly dwindling pipeline of projects to unprecedented levels of government support for the industry.

From June 4 2020, the federal government’s ‘HomeBuilder’ program provided a $25,000 grant for eligible new builds and large scale home renovations on homes that met the government’s criteria. According to the federal Treasury as of March 2022, HomeBuilder had cost a total of $2.1 billion and received more than 137,000 applications (113,113 for new builds and 24,642 for renovations).

According to an analysis from Master Builders Australia, the value of building work supported by HomeBuilder amounted to $41.6 billion.

Various state and territory government grants for new homes also helped increase the number of new homes under construction to all time record highs.

Meanwhile, as the way Australians live and work changed dramatically as a result of the pandemic, demand for home renovations surged. According to the ABS during 2021 Australians spent $12.3 billion on renovating their homes, up 33 per cent compared with 2020.

Amid all this stimulus and pandemic driven activity, the construction sector has at times suffered from materials and labor shortages as it attempted to keep pace with rising demand.

But with HomeBuilder and various state and territory grants now in the rear view mirror, a concerning picture of the future is now slowly emerging.

Concerning signs

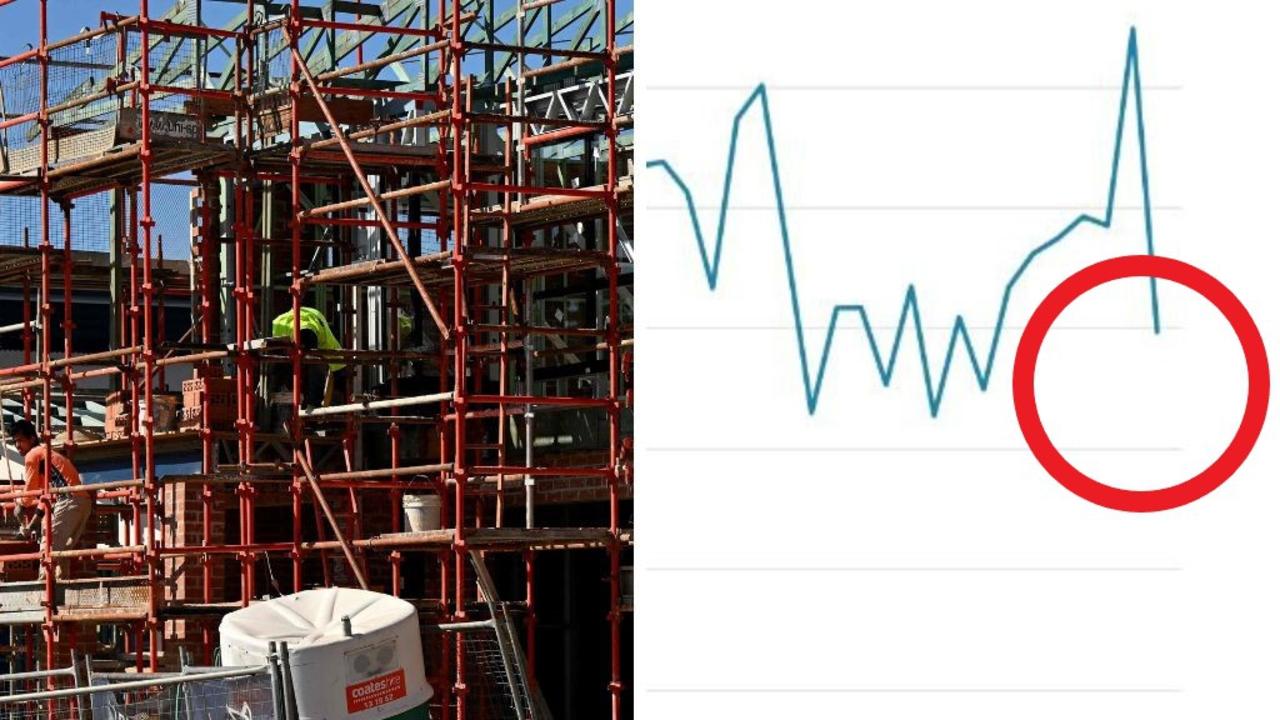

Since peaking in March 2021, dwelling approvals have failed by 29 per cent as of the latest data for June this year. After hitting an all-time record high in June 2021, dwelling commencements are following approvals down, falling 27.5 per cent as of the March quarter.

While a relatively strong pipeline of work remains and tradies are still in huge demand across much of the nation, the various forward looking indicators for the industry are showing similar concerning signs to those displayed in 2019.

However, unlike 2019 the broader economic circumstances are quite different and there are risks that the fortunes of the construction sector could deteriorate more swiftly. With mortgage rates currently rising at their most rapid relative rate in Australian history and inflation tipped by Treasury to hit 7.75 per cent by the end of the year, in time Australians may be much more reticent to take the plunge and pull the trigger on building a brand new home.

In 2020 the construction sector became the latest example of the “Lucky Country’s” good fortune coming to the rescue at exactly the right time. But now with a very different backdrop of economic circumstances, the sector has become even larger and activity levels even higher than the previous peaks, from which the RBA and UBS warned that the falls from could prove quite challenging.

Ultimately, despite the deteriorating forward looking indicators it is still very much early days for the construction sectors eventually slow down. More government stimulus or social housing construction may yet still come to somewhat fill the gap, but whether the sectors good fortune will hold, remains very much up in the air.

Tarric Brooker is a freelance journalist and social commentator | @AvidCommentator

.