WA’s biggest independent food distributor has warned consumers to expect further hikes at their favorite pubs and restaurants – and eventually supermarkets – as supply chain pressures and skyrocketing input costs continue to drive up prices.

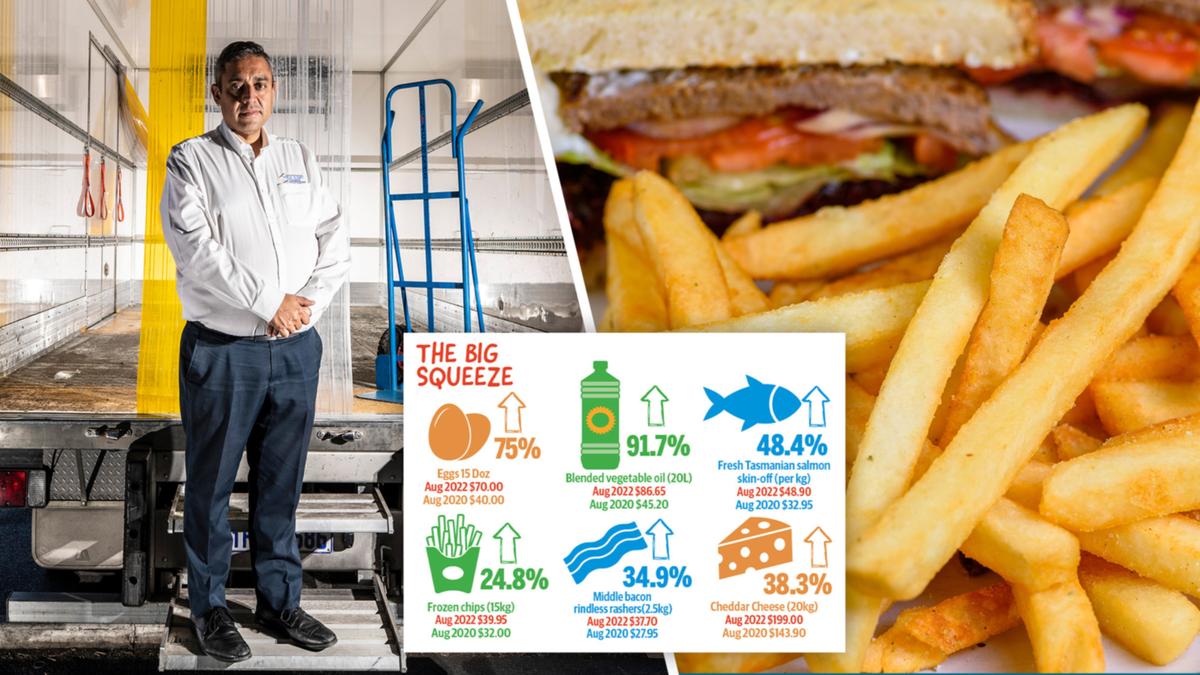

The price of vegetable oil supplied by New West Foods to hundreds of eateries across WA has almost doubled since August 2020, with eggs up 75 per cent over the same two-year period.

Salmon has jumped 50 per cent while cheese and bacon are both up around 35 per cent.

Even the humble frozen chip – a staple of takeaway menus everywhere – has climbed 25 per cent.

The scale of price rises over the past two years. Credit: The West Australian

The majority of those price rises have come in the last 12 months as myriad factors combined to create what New West Foods managing director Damon Venoutsos said was the “perfect storm” for food costs.

Mr Venoutsos described distribution businesses like his own as the “canary in the coal mine” for price increases because – unlike supermarkets and fast-food chains – they did not enter into long-term agreements with suppliers.

“Most of the time we get 30 days’ notice from our suppliers that prices are going up whereas your big retailers (such as Coles and Woolworths) and quick service restaurants (such as KFC) can lock in their prices for anything up to six months ,” he said.

“Often we’re using the exact same supplier so while I don’t know when (the supermarkets) are going to catch up, it’s inevitable they will have to.”

Mr Venoutsos said prices had increased “very quickly and very dramatically” in recent months and that practically no food type had been spared, although some – such as fish, meat and dairy – had been impacted worse than others.

The biggest riser – vegetable oil – is in short supply globally, with exports largely cut off from war-torn Ukraine which traditionally produces 50 per cent of the sunflower oil used around the world.

New West Foods clients include Optus Stadium, King Edward Memorial and Sir Charles Gairdner hospitals and hundreds of restaurants and cafes.

New West Foods managing director Damon Venoutsos has warned of more price hikes. Credit: simon santi/The West Australian

Mr Venoutos said takeaway-oriented restaurants such as fish and chip shops and pizzerias were among the hardest hit with practically all their staple ingredients surging in price.

Independent Food Distributors Australia chief executive Richard Forbes listed half a dozen reasons for the escalating costs including clogged ports globally, COVID lockdowns in China, a shortage of sea containers and spiraling domestic energy and transport prices.

Last month, Manjimup-based WA Chips – the State’s only local manufacturer – revealed its gas bill was up $400,000 (60 per cent) compared to the previous year.

Mr Forbes said additional costs were being incurred at every step of the production, distribution and storage supply chain.

“Anyone that refrigerates product in bulk – which would be practically all distributors – have seen those costs go from around $50,000 to $80,000,” he said.

Labor shortages were also a major issue, with Mr Forbes estimating there were 160,000 vacancies between the agriculture, transport, warehousing and hospitality sectors.

As the Reserve Bank raises interest rates for the fourth time in four months, home loan borrowers are bracing for more repayment pain.

Key points:

Banks are offering big discounts to new home loan customers

The number of borrowers refinancing their home loans is at a record high

Borrowers are shying away from more expensive fixed-term mortgages

The official interest rate is now at its highest level in six years, at 1.85 per cent, up from a record low of 0.1 per cent at the start of May.

Some economists say the RBA is only halfway through its rate-hiking cycle, with the goal of reaching, or even exceeding, 3 per cent by the end of the year.

As the cost of money goes up, the big four banks have dramatically raised interest rates for existing customers with variable-rate loans, and more rate rises are expected.

RateCity said bank customers could expect to see an average variable rate of 4.61 per cent if today’s RBA rate rise was passed on in full.

It said the accumulated 1.75 per cent rise in borrowing costs that had occurred since early May would add an extra $472 a month to mortgage repayments for the typical borrower with a 25-year, $500,000 loan.

Borrowers with a $1 million mortgage would have to pay an extra $944 a month.

RateCity’s estimate of the cost of RBA rate rises on monthly mortgage repayments. (RateCity: Supplied)

Fixed rates are rising

The rates offered for new fixed-rate loans are rising noticeably.

It comes as new Australian Bureau of Statistics (ABS) data show the proportion of new home loans being written with fixed rates has plunged to 9 per cent, down from the July 2021 peak of 46 per cent.

Sally Tindall, the research director at RateCity.com.au, said 90 lenders raised rates on fixed-term home loans last month before this latest increase.

“Fixed-rate hikes are coming thick and fast as the cost of funding continues to put pressure on the banks’ bottom line,” she said.

The financial comparison service Mozo said the fixed rates offered by some online lenders had already emerged to as high as 8 per cent.

As of Tuesday evening, no major bank had announced an interest rate increase in response to RBA’s latest rate hike.

But Macquarie Bank announced a range of different price responses.

It said it would increase its variable home loan reference rates by 0.5 per cent from 12 August.

It will decrease its fixed-home-loan interest rates by up to 0.75 per cent for new customers and existing variable-rate customers who want to fix their interest rate, from 5 August.

And it will increase the ongoing interest rate on its savings and everyday transaction accounts by 0.5 per cent, to 2.25 per cent, on balances up to $250,000.

Refinancing arises, demand for new loans weakens

As the higher cost of borrowing sees demand weakening for new home loans, more existing borrowers are refinancing to try to eke out lower interest rates from their banks’ competitors.

Mortgage broker Mortgage Choice said 42 per cent of borrowers who took out home loans in June were refinancing existing debt.

Discounts offered by banks for new borrowers saw refinancing jump 9.7 per cent in June to a record $12.7 billion.

Meanwhile, the value of new loan commitments being written each month remains near historically high levels, but it is clearly on the decline.

The ABS said the value of mortgage approvals fell by 4.4 per cent in June, on a seasonally adjusted basis, as the RBA’s rate hikes dampened appetite for borrowing.

The value of new loan commitments remains at an historically high level, but it is starting to fall away.(Source: Australian Bureau of Statistics)

“The value of new owner-occupier loan commitments fell 3.3 per cent in June 2022, while new investor loan commitments fell 6.3 per cent,” Katherine Keenan, ABS head of finance and wealth, said.

“These falls followed rises in May, attributed to a clearing of application processing backlogs by lenders.”

Discounts offered for lower-risk borrowers

Research from financial comparison website Canstar shows almost one in two lenders are offering loans with slightly lower rates to borrowers with large deposits.

It says for borrowers with a 40 per cent deposit or the equivalent equity in their property, 49 per cent of lenders on its comparison site are offering interest rates that are on average 0.21 per cent below the rate being paid by borrowers with a half deposit that size.

Canstar financial analyst Steve Mickenbecker said as the economic outlook became more uncertain, lenders were competing harder for lower-risk borrowers.

“Property prices are widely expected to fall by 10 per cent to 20 per cent,” he said.

“Lenders are looking for loans where there is a greater buffer for falls in property prices and almost half of them are rewarding these borrowers with lower interest rate offers,” he said.

“Having enjoyed strong house price increases over the last couple of years, borrowers who have been in their houses for several years now own a healthy share.

“There may be a strong case for borrowers in this position to open up a negotiation with their lenders for a rate reduction,” he said.

Late last month, ANZ reduced rates on new standard variable mortgages by up to 0.5 percentage points for borrowers with bigger deposits.

Ms Tindall told RN Breakfast that it paid for people to shop around, with 10 lenders cutting rates for new customers over the past three months.

“What we do know from all the data that comes through is that new customers, customers willing to switch to a different bank, often get the best deals,” she said.

“Why? Because banks discount rates for new customers, not loyal existing ones.”

The $739 billion Democratic spending plan dubbed the Inflation Reduction Act will barely affect prices over the next decade, experts say — and even the White House admitted it Monday.

According to Moody’s Analytics chief economist Mark Zandi, the 725-page bill hammered out by Sens. Chuck Schumer (D-NY) and Joe Manchin (D-WV) would only lower the Consumer Price Index – a closely watched gauge that measures what consumers paid for goods and services –0.33% by 2031.

“Through the middle of this decade the impact of the legislation on inflation is marginal, but it becomes more meaningful later in the decade,” Zandi wrote.

Jesse Lee, a senior communications adviser to the National Economic Council, was quick to tout Zandi’s findingstweeting, “This is actually the overwhelming consensus.”

“White House officials’ own rosiest, best-case-scenario spin is that their ‘Inflation Reduction Act’ will have taken one third of one percentage point off inflation by nine years from now?” Andrew Quinn, a speechwriter for Senate Minority Leader Mitch McConnell (R-Ky.), asked incredulously.

“White House comms spiking the ball over a bill that doesn’t reduce inflation until 9 years from now,” mocked Heritage Foundation spokesman Jon Cooper. “And keep in mind, this is obviously the best number they could come up with.”

The White House admitted the Inflation Reduction Act from Sens. Joe Manchin and Chuck Schumer won’t impact prices much over the next decade.Photo by Anna Moneymaker/Getty Images

Schumer and Manchin have claimed the bill would reduce inflation by lowering prescription drug and energy costs while reducing the federal budget deficit through a 15% minimum tax on corporations that report income of at least $1 billion per year, and increased tax enforcement by the IRS, and increased tax enforcement by the IRS. taking a share of profits earned by general partners at private equity, hedge funds, and venture capital firms known as carried interest.

However, experts say the inflation cure prescribed by the Democrats is likely to be ineffective, and could be worse than the disease.

Alex Muresianu, a federal policy analyst with the Tax Foundation, told The Post on Monday that the corporate tax – also called the “book minimum tax” — would “reduce supply in the long-run by reducing incentives to invest, particularly for manufacturing firms .”

“Meanwhile, on the demand-side, by taking money out of the economy, tax increases in excess of the spending attached could reduce inflation incrementally, but there are a couple problems,” he added. “First, in the first couple years, the bill does not net reduce the deficit — most of the net reduction in the deficit over the ten-year window comes in later years.

Schumer and Manchin claimed the bill would lower prescription drug and energy costs. Photo by Drew Angerer/Getty Images

“And second, the tax increases like the book minimum tax are not focused on taxpayers with high marginal propensity to consume, meaning the tax increase does not come with a particularly large reduction in aggregate demand.

“So, on the whole,” Muresianu concluded, “we should expect the bill to have a negligible impact on inflation. The Federal Reserve’s choices will play a much bigger role in whether or not inflation subsides than whether or not this bill passes.”

Levon Galstyan, a Certified Public Accountant with Jersey City-based Oak View Law Group, agreed, noting: The Inflation Reduction Act will shift resources through hundreds of billions of dollars in special-interest subsidies targeted to Democratic constituencies, further limiting supply through restrictions and tax increases.

“A deterrent to output would be that manufacturers would pay around half of all new levies,” Galstyan also told The Post. “The legislation would subject small businesses to a horde of tax enforcers, driving up prices and limiting their capacity to serve customers.”

According to Moody’s Analytics chief economist Mark Zandi, the bill would only lower the Consumer Price Index by 0.33% by 2031.AP Photo/Alex Brandon

Peter Morici, an economist and professor emeritus at the RH Smith School of Business at the University of Maryland, also argued that there was almost no chance the legislation would reduce prices.

“One of the Fed bank presidents [Neel Kashkari of Minneapolis] came out [Sunday] morning … saying we’re going to get inflation down at 2%. If you believe that, then I want you to go to Yankee Stadium on Sunday afternoon and look for me playing shortstop,” Morici told The Post.

“I’m 73 years old. I was a pretty damn good middle infielder, but I didn’t have much of a career because I never could hit the breaking ball,” he added. “I mean, that’s as credible as I’m gonna play shortstop for the New York Yankees.”

Other experts have pointed out that the legislation fails to provide a long-term solution for bringing down inflation.

“Inflation results from deep-set, fundamental issues and this bill does nothing to address those factors,” said James Lucier, managing director at Washington-based policy research firm Capital Alpha.

Biden administration official Jesse Lee, a senior communications adviser to the National Economic Council, agreed with Zandi’s findings.AP Photo/Susan Walsh

“Inflation will probably fix itself over a ten year period, if we’re lucky,” Lucier told The Post, labeling the supposed “anti-inflationary effects” of the legislation as “smoke and mirrors.”

Rather than bringing down prices, some of the economists suggested that federal tax credits for Americans to buy electric vehicles and the extension of ObamaCare subsidies would exacerbate the problem.

“They’re giving people money to buy electric vehicles. They’re in short supply. The lithium that goes into them is in short supply. That’s gonna raise the price of electric vehicles,” said Morici, who added that “additional subsidies to buy health insurance is not going to lower the cost of health insurance, it’s going to increase the price.”

“Many of the incentives that are in the bill tend to increase the price of components for products that go into the electrical grid and so forth,” Morici continued. “So it’s basically giving people money to chase products that are in short supply.”

Will McBride, VP of federal tax and economic policy at the Tax Foundation, echoed that concern, saying the ObamaCare subsidies would make “entitlement spending” worse.

“Essentially,” McBride said, “the value of the dollar is getting diminished as the federal government’s ability to repay its debt diminishes.”

Additional reporting by Lydia Moynihan and Ariel Zilber.

New Zealand’s borders fully reopened to visitors from around the world on Monday, for the first time since the COVID-19 pandemic closed them in March 2020.

Key points:

New Zealand will welcome all international travelers from July 31

Jacinda Arden says the final stages included welcoming back those on student visas and letting cruise ships and foreign yachts dock in the country

The country imposed some of the world’s strictest border controls when COVID-19 first hit

The country started reopening in February, first for New Zealanders returning home, and restrictions have progressively eased.

The process of reopening the borders ended last night with visitors who need visas and those on student visas now also allowed to return.

New Zealand is now also letting cruise ships and foreign recreational yachts dock at its ports.

International students were a significant contributor to New Zealand’s economy and educational providers are hoping the reopening of the borders will again provide a boost to schools and universities around the country.

Space to play or pause, M to mute, left and right arrows to seek, up and down arrows for volume.

New Zealand’s border opening plan revealed by Prime Minister Jacinda Ardern

Prime Minister Jacinda Ardern said on Monday during a speech at the China Business Summit in Auckland that the final staged opening of the borders had been an enormous moment.

“It’s been a staged and cautious process on our part since February as we, alongside the rest of the world, continue to manage a very live global pandemic, while keeping our people safe.”

Opening provides relief for Australia

Pre-COVID, Australia and New Zealand citizens had enjoyed free movement between the two countries since the 1920s.

But for the past two years, New Zealand imposed some of the world’s strictest border controls, which led to headaches for the hundreds of thousands of NZ citizens living in Australia.

As of mid-2018, there were an estimated 568,0000 New Zealand-born people residing in Australia — representing the fourth-largest migrant community.

Economically, tourism was New Zealand’s largest export industry and a huge proportion of their tourists were Australians before the pandemic hit.

Some four in 10 visitors to NZ are from Australia.(Pixabay: Michelle Rapon)

Almost one in 10 New Zealanders were directly employed in tourism and there were 1.5 million arrivals from Australia — accounting for 40 per cent of international visitors to NZ in 2019 — who spent some $NZ2.7 billion ($2.5 billion).

And it went both ways — New Zealanders were the second largest market for visitor arrivals into Australia in 2019.

New Zealand has been slowly reopening, first to Australians in March and then to tourists from the US, Britain and more than 50 other countries in May.

Australians face a big rise in the cost of a pint, with the country’s beer tax recording its biggest increase in more than 30 years.

As of Monday August 1, the beer tax goes up to 4 per cent, adding about 80-84 cents to the cost of a pint of the much-loved amber liquid. This means you may soon be paying $15 for your favorite glass.

And there’s no escape for those who buy their beer by the slab. The beer tax will rise from $53.59 to $55.73 per liter of the beverage’s alcohol content, raising the tax on a carton about 80c, to $18.80.

Watch the latest News on Channel 7 or stream for free on 7plus >>

The tax on a keg will jump about $4, raising the cost to almost $74.

Because of this price hike, Brewers Association of Australia chief executive John Preston warned that patrons might now have to fork out $15 for a pint at their local pub or bar.

“For a small pub, club or other venue the latest tax hike will mean an increase of more than $2700 a year in their tax bill – at a time when they are still struggling to deal with the ongoing impacts of the pandemic,” he said .

The biannual alcohol excise is based upon the consumer price index (CPI), which is a measure of the average change over time in the prices paid by households for a fixed number of goods and services.

According to the ABS, the June CPI increased by 6.1 per cent over the last 12 months, with goods accounting for 79 per cent of the rise this quarter.

Due to the tax increase, patrons may now have to pay $15 for a pint at their local pub or bar. Credit: Getty Images

Publican of the Royal Albert Hotel in Sydney’s Surry Hills, Michael Bain, said that while the increase was certainly high, beer tax increased twice a year every year (in February and August), meaning the issue isn’t a particularly new one.

“These price rises … just keep affecting us all the time,” he said.

“Because of COVID, I think a lot of people didn’t put the excise on…so I think this is why it’s affected us more this time.

“Especially some of the craft brewers that we use, they’ve been absorbing those CPI increases. But even the small guys now are going to have to pass it on, so it will mean a price rise across the board for us.”

Preston said the industry had seen “almost 20 increases in Australia’s beer tax over the past decade alone”.

“Australians are taxed on beer more than almost any other nation,” he said.

If patrons are forced to pay $15 for a pint of beer, Bain said he believes people will still buy it, but may buy fewer beers.

“Instead of buying three beers, they’ll buy two. I think they really will buy one less,” he said.

Federal Treasurer Jim Chalmers. Credit: AAP

According to Preston, breweries and pub and club operators were “extremely disappointed” when the former government did not deliver its proposed beer tax reduction in this year’s budget, and that the new Treasurer, Jim Chalmers, has now “inherited” the Liberals’ problem .

“We believe there is a strong case for beer tax relief to be provided by the new federal government, with the hidden beer tax to go up again in February 2023,” he said.

Bain agrees, saying another possible solution could be cutting down the tax from twice a year to once a year.

“I’m not saying they shouldn’t do it and we need to pay taxes for health care and all that kind of stuff, but at what point do you just keep gouging everyone?

“You can’t keep incrementally adding on all the time at these massive rates

“(It’s) kinda like you’re absolutely smashing people with tax.”

Sen. Joe Manchin in the US Capitol on Tuesday, June 14, 2022. Sen. Joe Manchin, DW.Va., and his staff told Democratic leadership on Thursday that he’s not willing to support better climate and tax provisions in a sweeping Biden agenda bill, according to a Democrat briefed on the conversations.

Tom-Williams | Cq-roll Call, Inc. | Getty Images

Senator Joe Manchin, DW.V., made the morning talk show rounds on Sunday to talk about the Inflation Reduction Act of 2022, a revival of President Joe Biden’s Build Back Better economic bill that collapsed earlier this year.

The inflation bill, which Democrats are attempting to pass through reconciliation, aims to reform the tax code, cut health-care costs and fight climate change. It will invest more than $400 billion over a decade by closing tax loopholes, mostly on the largest and richest American corporations. It would also reduce the deficit by $300 billion in the same decade-long timeframe.

“This is all about fighting inflation,” Manchin told Jonathan Karl on Sunday’s “This Week” on ABC.

Manchin insisted that the bill isn’t a spending bill, but instead is focusing on investing money.

“We’ve taken $3.5 trillion of spending down to $400 billion of investing without raising any taxes whatsoever, we closed some loopholes, didn’t raise any taxes,” he added.

He further explained the closing of tax loopholes, which will raise taxes on certain American companies. Any tax increase could jeopardize full Democratic support of the legislation, which it needs to pass through reconciliation – Senator Kyrsten Sinema, DA.Z., may not support this provision.

“The only thing we have done is basically say that every corporation of a billion dollars of value or greater in America should pay at least 15% of minimum corporate tax,” he said on NBC’s “Meet the Press.”

“That’s not a tax increase it’s closing a loophole,” he said.

Manchin also noted that a deal between Senate Majority Leader Chuck Schumer, D-NY, and he was struck in private to avoid drama.

“We’ve been negotiating off and on very quietly because I didn’t know if it would ever come to fruition,” he said. “I didn’t want to go through the drama that eight months ago we went through for so long.”

Manchin added that he’s struck an agreement with Democratic leaders to support the bill in exchange for taking on permitting reform later.

“If I don’t fulfill my commitment promise that I will vote and support this bill with all my heart, there are consequences, and there are consequences on both sides,” he said on “Meet the Press.”

Manchin also noted that the bill will especially target energy prices in the US by upping production and using clean energy effectively.

“Inflation is the greatest challenge we have in our country right now,” he said on CNN’s “State of the Union.” “If you want to get gasoline prices down, produce more and produce it in America.”

manchin dodges election talk

During his Sunday interviews, Manchin repeatedly evaded answering questions about who he supports in upcoming elections – the 2022 midterms and the 2024 presidential election.

“I’m not getting involved in any election right now,” he said on “State of the Union.”

He reiterated that he would work with anyone that voters elect and specifically wouldn’t answer if he wants Democrats to keep control of Congress come November.

“Whatever the voters choose,” he said on “Meet the Press.” “Whoever you send me that’s your representative and I respect them.”

When specifically asked if he’d support Biden in reelection, he focused on Biden’s current presidency.

“Whoever is my president, that’s my president, and Joe Biden is my president right now,” he said on “This Week.”