What Gandhi calls prudence – disappearing the proceeds of new shares into operational expenditure – is more commonly known as capital ill-discipline, though investment bankers just call it a dream client.

The placement’s co-underwriters, Citi and JPMorgan, know each other well, having performed the same roles on ANZ Banking Group’s $2.5 billion placement in 2015 – subject of the ACCC’s blockbuster cartel case only abandoned in February. It’s fair to say the two ECM desks will be choosing their words very carefully if any demand shortfall leaves them with surplus Orica stock.

Languishing through a bull run

Orica bussed more than 40 analysts and fund managers to the Hunter Valley last week for a site tour of its technical center in Kurri Kurri to beguile them with the company’s (age-old) technology narrative. That lucky crew learned on Wednesday morning there’s no such thing as a free lunch.

On completion of the latest raising, there will be 19 per cent more Orica shares on issue than there were in October 2019, and over the same period (based on consensus for FY22) earnings before interest and tax will have failed by 19 per cent. Dividends are down 38 per cent. What are these outputs if not fundamental to the underlying business?

From the global financial crisis to COVID-19 and beyond, Orica has languished right through the bull run in Australian equities and the corresponding boom in resources investment. It’s some feat when your only real job is to deliver explosives to mine sites.

It was the legendary bully Ian Smith who privately described Orica as a blancmange; the harder you try to beat it into shape, the more resolutely it wobbles back to its original form – namely sprawling and unfocused.

Smith’s predecessor, Graeme Liebeltbought mining chemicals company Minova from a British private equity group for $857 million in 2006 and bolt maker Excel for $775 million the following year.

Minova and Excel were folded into a new ground support division and in August 2015, Orica impaired the carrying value of that division by $850 million. In December, Orica finally managed to sell it to German asset manager Aurelius for just $180 million.

And yet here Orica goes again!

In recognition of his magnificent record of capital allocation, Liebelt was appointed to the board of ANZ Banking Group in 2013, where he remains, contributing to the dissolute oversight of Shayne Elliott‘s own era of value destruction. How good is Australia?

When you picture an Audi you might imagine a high-priced luxury SUV such as the $150,000 Audi Q8 or a ferocious performance car like the circa-$250,000 Audi RS6 Avant, but the Audi A3 is a much more accessible machine.

Prices start at about $52,000 drive-away for the base 35 TFSI Sportback variant and rise to about $60,000 for the 40 TFSI version we tested.

It has flamboyant 18-inch alloy wheels, LED lighting and S-Line sporty styling pack.

Inside, owners are treated to leather appointed seats, a fully digital dash with a crisp, high-res sat nav display and ambient cabin lighting.

Manually adjustable seats and no radar cruise control are a let-down.

ITEMFEELS VERY FAMILY

Audi is part of the giant Volkswagen Group that builds vehicles across a range of brands including VW, Skoda and Bentley, and many of its cars share their underpinnings with a wide range of vehicles.

The A3 is built on the same platform as the Volkswagen Golf, Skoda Octavia, Audi Q3 SUV and the soon to arrive Cupra Formentor.

They all share many components including engines, transmissions and digital screens.

Audi has applied its own styling and finesse to the A3 to make it feel and look different, but the end result is a VW Golf from another dimension.

IT GOES

The base example scores a 1.5-liter turbocharged petrol engine that makes 110kW and 250Nm. The 40 variant we had gets a bigger 2.0-liter unit making 140kW and 320Nm and adds all-wheel drive traction instead of front-wheel drive.

The extra power and grip drops the 0-100km/h time from 8.4 seconds to seven seconds flat.

Audi claims the 40 TFSI will drink 6.7L/100km, which isn’t too shabby for a small car with a bit of grunt.

If this all sounds too pedestrian for you then the S3 is the go. It uses a powerful 2.0-liter turbocharged petrol engine making 228kW and 400Nm to deliver a 0-100km/h sprint time of just 4.8 seconds. A-soon-to-arrive Audi RS3 turns the dial all the way up.

IT’LL MAKE YOU SMILE

The A3 Sportback shows why those who love to drive chose a hatchback or sedan over an SUV.

Its lower ride height and weight make the A3 more composed on the road.

Firmish suspension, all-paw grip and light and fast steering make for an entertaining drive on a back country road.

It feels brisk off the mark and zippy in traffic and has no problems bounding up steep hills or overtaking on the highway.

The dual-clutch auto can take a minute to decide what it wants to do when you put your foot down so be aware when attempting to punch through tight gaps at intersections.

YOU’VE GOT OPTIONS

The Audi A3’s price is enticing, but when you look deeper you might find you’ll need to tick a few boxes to get the car you really want.

Metallic paint will set you back $1250, 18-inch Audi Sport alloy wheels add a further $500 and a premium Bang and Olufsen is another $1500.

If you want electronically adjustable and heated front seats, radar cruise control, a head-up display that projects vital information onto the windscreen and sharp looking aluminum interior inserts you’ll need to pony up an extra $4500.

If a hatchback isn’t for you, then you can have the A3 in a sedan body shape that adds about $2000 to the price of the 40 TFSI.

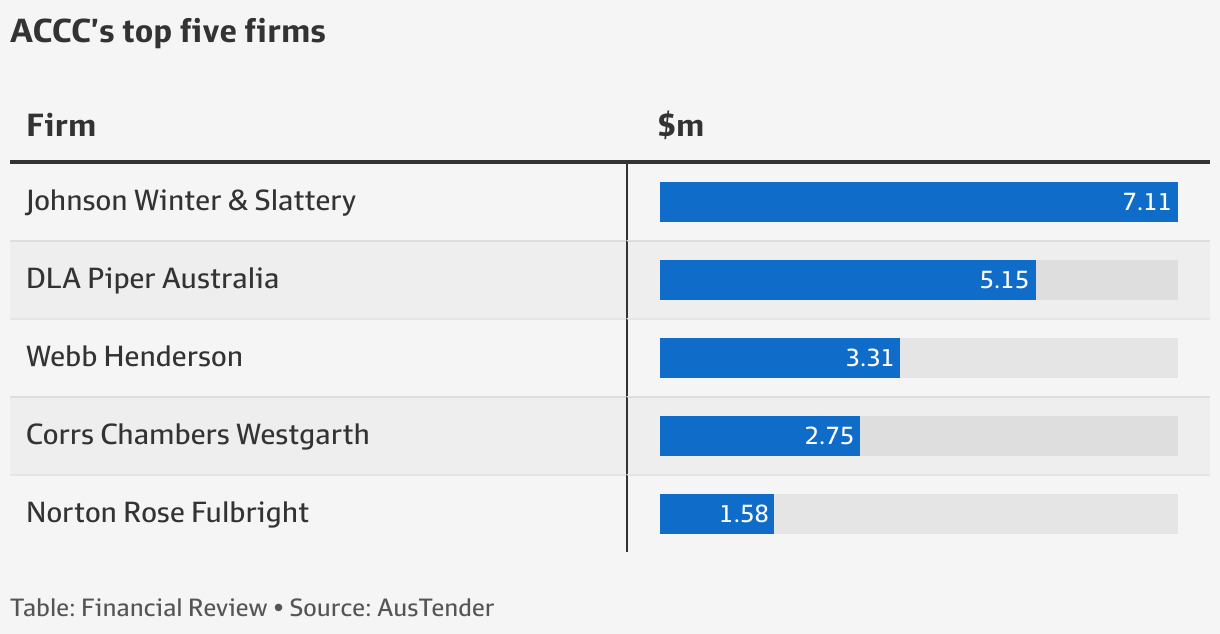

“If you don’t have that deep specialist expertise, you can’t run cases at this scale … we’ve got quite a deep competition practice and deep corporate regulation practice, and I think that’s what’s really resonated with the regulators, Mr Davis told The Australian Financial Review.

This allowed the firm to tap into the boom in ASIC litigation work since the Hayne royal commission and the jump in ACCC cases under its former chairman, enforcement enthusiast Rod Sims.

Unlike other corporate players, Mr Davis said JWS was willing to work with watchdogs and the companies they oversee, and was less concerned about keeping poachers onside by refusing to work for gamekeepers.

“We haven’t chased high-volume commercial bank panel work,” he said. “We chase complex work, and whether that’s for the ACCC or ASIC or a client like Unilever, if it’s interesting, high-level work it’s something we want.”

Mr Davis pointed to the firm’s recent work for ASIC against Westpac, which many other firms could not do because they either had conflicts or did not want to risk damaging their relationship with the big four institution.

JWS announced on Thursday it would open a Canberra office to assist private companies needing to deal with government.

King & Wood Mallesons was the go-to firm for the prudential regulator, though only about $300,000 of KWM’s almost $40 million in federal government contracts came from regulatory work.

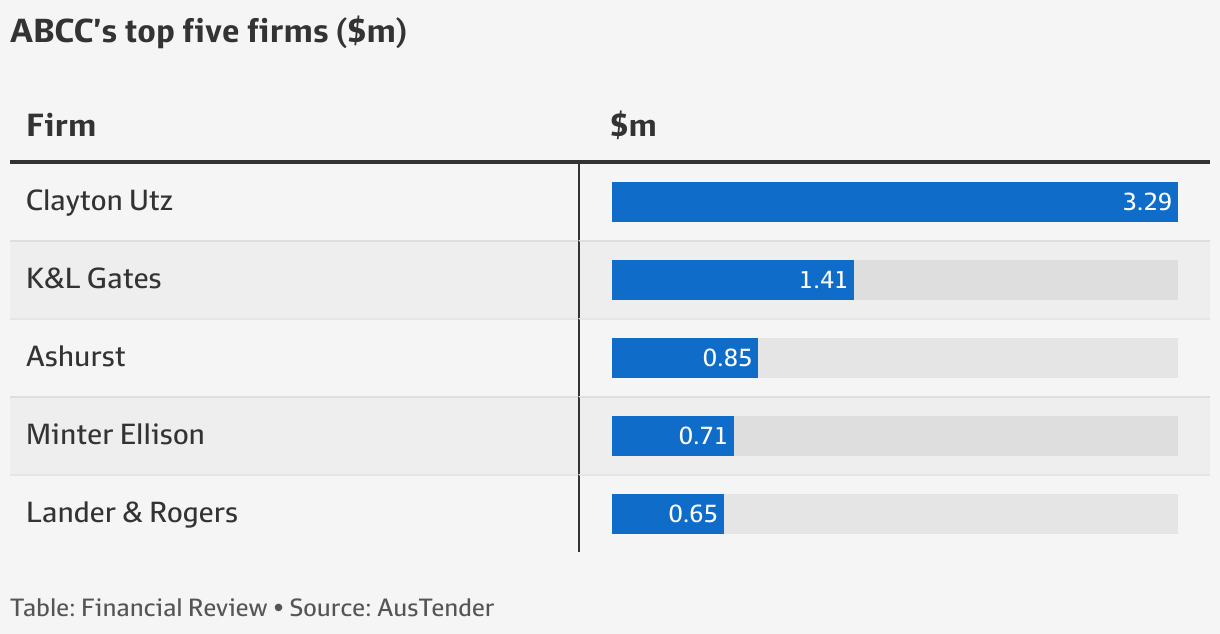

Clayton Utz was the top adviser to the controversial Australian Building and Construction Commission. The top-tier independent inked deals worth $3.2 million last financial year, just under half the ABCC’s $7.1 million spend.

Labor announced last week it was moving to abolish the building watchdog, which it accused of wasting taxpayer money on attacking unions.

KWM earned the No.1 spot with $39.2 million in government contracts in 2021-22. It was followed by Sparke Helmore ($31.9 million), Norton Rose Fulbright ($29.4 million), Clayton Utz ($28.7 million), and Ashurst ($24 million).

Norton Rose’s continued rise through the rankings – up from fifth position last year – is part of a major push by the global firm into Canberra that began with the poaching of three partners in 2018 from Sparke Helmore.

After securing about $10 million worth of work from the Tax Office and ACCC in 2020-21, the firm’s biggest client in contract value last financial year was the Defense Department, from which it secured $14.7 million in work.

MinterEllison ranked sixth with $22 million in contracts booked, down from $32 million last year, however this was largely due to major client the Tax Office locking in a multi-year deal that ran through June 20, 2022 (which showed up in last year’s rankings but does not flow this year).

Defense biggest spender

The Defense Department was again the biggest spender on external law firms, with $45 million in contracts commencing last year, followed by Finance ($28 million), the ACCC ($25.4 million), the Attorney-General’s Department ($24.8 million), and Health and Aged Care ($17.5 million).

All up, federal government departments signed contracts with the top 20 law firms worth slightly more than $247 million.

the Financial Review annual rankings of law firm government work is based on AusTender contracts published by August 1 that commenced in 2021-22. Contracts often run over multiple years, but the value is only recorded in the commencement year.

Data on the AusTender website is updated regularly and may change over time, and contracts are often only indicative of billing agreement values; the final level of work billed may be higher or lower as required.

Another 135 Hyundai Ioniq 5 electric cars will go on sale next Wednesday, for capital city buyers in nearly all states and territories.

0

Another batch of 2022 Hyundai Ioniq 5 electric cars will become available to order next Wednesday, August 10.

Hyundai Australia confirmed today the next Ioniq 5 allocation – the seventh since the car went on sale last September – will open at 1:00pm AEST on August 10, for buyers in the capital cities of all states and territories except the Northern Territory.

The latest batch will comprise 135 cars – the most of any since the initial 240 released last September, though given Hyundai Australia sells every car it makes available, supply is still outstripped by demand.

Both entry-level, rear-wheel-drive Dynamiq 2WD and flagship, all-wheel-drive Techniq AWD variants will be available to purchase, with the higher grade including a glass ‘Vision Roof’ as standard.

As with prior allocations, the August 10 vehicles are expected to be pre-built – though a mix of colors and model grades is expected to be offered.

Hyundai Australia says buyers in the latest allocation should expect to take delivery “within two months” – indicating the final arrivals by mid October.

Hyundai’s system of releasing a small batch of Ioniq 5s every month is intended to cut wait times – in contrast to the two-year wait that faces buyers of the related Kia EV6 – and ensure buyers in applicable regions have an equal chance of securing a vehicle .

Pricing and specifications for the latest batch were revealed last month, with an entry-level Dynamiq grade from $69,900 plus on-road costs, or a top-of-the-range Techniq from $77,500 plus on-road costs. Click here for more details.

Every Hyundai Ioniq 5 allocation in Australia so far

Date

States/cities included

variants

Number of cars

Read more

Late September

All states and territories

All (RWD and AWD)

240

Details

16 December 2021

Sydney and Canberra

All (RWD and AWD)

90

Details

27 January 2022

Brisbane, Perth, Melbourne

All (RWD and AWD)

66

Details

23 March 2022

NSW, ACT, Victoria, Queensland, WA, SA and Tasmania

All (RWD and AWD)

100

Details

May 18, 2022

Sydney, Melbourne, Brisbane, Perth, Canberra, Adelaide and Hobart

All (RWD and AWD)

68

Details

20 July 2022

All states and territories except the NT

Techniq only

119

Details

August 10, 2022

All states and territories except the NT

All (Dynamiq 2WD and Techniq AWD)

135

N/A

Total cars made available since launch: 818

Alex Misoyannis has been writing about cars since 2017, when he started his own website, Redline. He contributed for Drive in 2018, before joining CarAdvice in 2019, becoming a regular contributing journalist within the news team in 2020. Cars have played a central role throughout Alex’s life, from flicking through car magazines as a young age, to growing up around performance vehicles in a car-loving family.

“It is remarkable that the price outcomes of other capacity markets do not appear to have been considered by ESB … the ESB should critically examine the price impact of capacity markets in jurisdictions such as France, the UK and Western Australia.”

loading

Under the ESB’s proposal, retail companies would make the capacity payments to energy generators, which means the cost would be passed on to households and businesses. The board said it would avoid higher bills.

“This is clearly not the intent, and it will be avoided through careful design,” it said.

As coal-fired power stations face mounting financial pressure from cheaper-to-run renewable energy slashing daytime electricity prices, the ESB is worried that abrupt closures could jeopardize reliability and cause volatile prices.

“Wholesale prices in Victoria jumped 85 per cent following the sudden closure of the Hazelwood power station before any replacement capacity could be built,” it said in a report in June.

However, wind and solar farm operator Tilt Renewables cited modeling extrapolating the cost of Western Australia’s capacity market to the east-coast grid, which suggested residential consumers could pay up to $6.9 billion more for electricity each year.

“We agree with the minister that a capacity mechanism must be focussed on new technology and storage,” Tilt said.

“Unfortunately, the capacity market designed by the ESB does not focus on delivering new technology or storage … instead, it is focussed on forcing electricity customers to pay billions of dollars in windfall bonus payments to existing generators.”

Tilt said the mechanism’s design could prompt a number of older coal-fired generators to decide to continue operating “for another year or two” beyond what they would otherwise have. As well, it could mean customers would pay existing generators that had no intention to exit the market to continue doing “exactly what they were going to do anyway”, Tilt added.

The debate over the proposed redesign comes after the east-coast energy market was thrown into chaos earlier this year, when a spate of coal-fired power plant failures collided with surging fossil fuel costs to push the wholesale electricity prices to their highest-ever levels .

After the Australian Energy Market Operator (AEMO) was forced to impose rarely used caps to halt runaway prices, many power generators said they could not remain viable and withdrew offers to dispatch into the grid, exacerbating the supply crunch. The situation led to AEMO seizing control of the market for the first time in history to stabilize supplies and avert the threat of blackouts in multiple states.

The Business Briefing newsletter delivers major stories, exclusive coverage and expert opinion. Sign up to get it every weekday morning.

While Melbourne real estate house Qualitas is the talk of the town thanks to its eye-watering mandate, rival MaxCap has gone one better.

MaxCap’s investments include a $97 million debt facility to Franze Developments’ Geelong Quarter in the regional Victorian city of Geelong.

Not to be outdone by Qualitas’ $700 million from ADIA, MaxCap is understood to have received a near $1 billion check from its now biggest client, Apollo Global Management.

Sources said MaxCap was looking to deploy the capital in the property credit market, providing construction facilities, first mortgages on land and the like, at a time when there’s no shortage of deals for credit funds.

It’s not surprising to see Apollo Global go big in property credit – it is the firm’s bread and butter globally. It’s also not surprising seeing it getting closer to MaxCap, with Apollo having taken aa 50 per cent stake in the Melbourne-based property financier last year.

But it’s interesting to see the sheer size of Apollo’s commitment, particularly at a time when analysts and property market watchers are fawning over Qualitas. The company’s shares are up nearly 40 per cent this week.

Qualitas announced on Monday that it had secured a $700 million investment mandate from the Abu Dhabi Investment Authority (ADIA), in a deal that could also see ADIA take a near 10 per cent stake in the manager.

The sovereign wealth fund’s mandate could increase to $1.7 billion if it took the maximum 9.9 per cent equity stake.

Russian shoppers queue for H&M as retailer prepares to shut down its Moscow store

Brands like H&M, Ikea and Nike have stopped operations in Russia due to the war

H&M has reopened stores to clear out its goods before leaving Russia for good

A customer said ‘how are we going to manage,’ and the closure was ‘awful’

The closure of Russian stores has cost H&M nearly £170m and affects 6,000 staff

By Mark Nicol Diplomacy Editor For The Daily Mail

Published: | Updated:

Snaking through a Moscow shopping center, shoppers wait to buy their last items from H&M before the retailer closes its Russian stores.

Brands including H&M, Ikea and Nike had suspended operations in the country, but H&M reopened to sell off its goods before leaving the Russian market for good, costing the company nearly £170million.

Customer Ekaterina said: ‘The reason why this is happening is awful. Everything else is meaningless, like how we are going to manage [without H&M].’

Russian shoppers wait to buy their last items from H&M in a Moscow shopping center before the retailer closes its Russian stores

‘The reason why this is happening is awful. Everything else is meaningless, like how we are going to manage [without H&M],’ a customer said. Pictured left: A customer at the closing H&M in Moscow. Pictured right: Shoppers stand in line to the entrance of the H&M store

‘Well, it is closing, that’s why we are standing here,’ another customer, Irina, told Reuters. ‘I’m going to buy whatever there is.’

Furniture giant IKEA has reopened for an online-only sale, but H&M opted to allow customers back in person.

Exiting Russia, H&M’s sixth-biggest market, is expected to cost the company almost $200 million and affect 6,000 staff.

Exiting Russia, H&M’s sixth-biggest market, is expected to cost the company almost $200 million (around £165m) and affect 6,000 staff

H&M did not immediately respond to a request for comment.

A company spokesperson in July said H&M would temporarily reopen physical stores in August to sell the remaining inventory in Russia.

H&M, the world’s second-biggest fashion retailer, rents its 170 physical stores in the country and operates them directly.

Australian Wagyu producers are unable to meet domestic and international demand as an appetite for the premium meat soars.

Irongate Wagyu, based near Albany in Western Australia’s Great Southern region, produces full-blood Wagyu, which can sell for as much as $450 per kilogram.

Managing director Peter Gilmore said interest in the company’s carcasses and genetics had tripled over the past 12 months.

“The increase is demand, I would say, is around 300 per cent,” he said.

“If we had three times the number of animals, we probably could not meet that demand.”

Irongate’s Peter Gilmore says there are about 1,000 breeders, 700 weaners and 500 feeder animals on farm.(ABC Great Southern: Angus Mackintosh)

Irongate sells genetics to Australian producers and Mr Gilmore predicts the domestic Wagyu industry will expand.

“On the animal production side, we have seen a very big uptick and a lot of people are purchasing … to try and obviously lift their own farm gate receipt — I mean, Wagyu produces a significant premium over the rest of beef production,” he said.

“I think the industry has the potential to actually, in the future, get up there with equal to Japanese production.”

The increased investment in Wagyu is not limited to the southern parts of the state.

Pardoo Beef Corporation, based in the north, has invested more than $75 million in its Wagyu operation.

Its Singaporean owner, Bruce Cheung, plans to run more than 100,000 head of cattle across the Pilbara and Kimberley by 2035 in a business worth $3 billion.

Nathan Robb was one of the first butchers to sell full-blood Wagyu in Western Australia.(Supplied: Nathan Robb)

Domestic demand sounds

Nathan Robb, the owner of Bullsbrook-based Bully Butcher, says he needs more than double what Irongate supplies him with to meet demand.

“We receive [the Wagyu] on a Monday, by the following Monday it’s gone,” he said.

“Everything is pretty much put on hold for customers in advance.

“In the last 12 to 18 months it has gone from a little bit of interest to almost every customer asking a question about it.

“A lot of people don’t know what it is, they see it and think, ‘Wow I wouldn’t mind trying that.'”

Mr Gilmore said that increase in domestic demand was correlated to a changed health focus.

“People understand that intramuscular fat can actually be good for you … I think there has been a real health focus shift and enjoyment for producing,” he said.

“If you go back two years when COVID first started, we had very little domestic output, almost nothing.

“Now domestic would be 40 per cent of our total production.”

Japan ceased releasing full-blood Wagyu genetics in the mid-1990s.(ABC Great Southern: Sophie Johnson)

Markets boom amid FMD threat

South-East Asian countries are asking for more Australian Wagyu because Japan is a selective exporter.

“Japan has a very satiated market,” Mr Gilmore said.

“They’re a net importer of meat, so they don’t really need to export.

“The international demand for Wagyu has been quite extraordinary over the past year, the amount of inquiry that has come in at a range of different levels from many different countries.

“There’s a Chinese demand which is enormous and certainly is the kind of demand that we would struggle with supply to meet.”

There are huge growth opportunities for Australian producers, but a disease outbreak could undo years of work.(ABC Great Southern: Sophie Johnson)

Scott Richardson, the managing director of producer and distributor Stone Ax Pastoral Company, says a foot-and-mouth disease outbreak could stop the trade in its tracks.

“If foot-and-mouth disease was introduced into Australia it would potentially decimate the Australian Wagyu beef breed, along with other elite genetics within the cattle breeding industry,” he said.

“It would particularly impact the full-blood Wagyu breed, given that Japan isn’t releasing any more full-blood Wagyu genetics.

“Australia would need to rebuild its herd with the genetics left on hand and what can be sourced internationally.

“It would take years and years to rebuild the herd to its current numbers.”

House prices have fallen by more than $100,000 in three months in parts of the country as rising interest rates reduce borrowing power and accelerate price declines.

Six-figure sums were wiped from median house prices in Sydney’s north shore, northern beaches and inner west, as well as Melbourne’s inner east, in the June quarter, Domain data shows.

Prices in parts of Brisbane, Hobart and regional NSW also pulled back more than $50,000. The median house price for the capital cities combined fell by less than $10,000 by comparison.

The sizable price falls came after the Reserve Bank began lifting the cash rate from a record low of 0.1 per cent in May. The declines are expected to spread, with a fourth consecutive rate hike on Tuesday, increasing the rate to 1.85 per cent.

READMORE: Real estate agency sprung “bragging” about a $225 per week price hike

Where property prices fell most for units, in dollar terms. (Domain)

Domain chief of research and economics Dr Nicola Powell said the cash rate increases had accelerated the slowdown, which was initially driven by an increased supply of homes for sale, affordability constraints, rising fixed-rate home loans and an increase to the interest rate serviceability buffer .

“Borrowing capacity has been eroded by higher rates and a higher cost of living … and there’s more to come in terms of a further acceleration in a deterioration in prices,” she said.

Median prices in premium markets had lost the most value, Powell said, which was to be expected, as the upper end typically led upswings and downturns.

In Sydney, prices dropped $250,000 in the north Sydney and Hornsby region, $200,000 in the inner west and $187,500 on the northern beaches. Prices in eastern suburbs held steady at median of $3.45 million but were down $200,000 year on year, due to price weakness in previous quarters.

House prices in Melbourne’s inner east dropped $107,500, while the median in Brisbane’s west fell $50,000.

READMORE: French manor set to break Queensland record with $35 million sale

Where property prices fell most for houses, in dollar terms (Domain)

Sydney’s eastern suburbs and the Baulkham Hills and Hawkesbury region led unit declines in dollar terms, down $90,000 and $55,000. Prices also dropped more than $55,000 in Hobart and the Coffs Harbor and Grafton region.

Powell said price declines would continue to spread. The full impact of rate hikes had yet to be seen, and buyer demand would be further tested by an expected increase in homes for sale in spring.

Home buyer lending pulled back in June after the second cash-rate rise. The value of new owner-occupier loans dropped 3.3 per cent, and was 9.6 per cent lower than a year ago, Australian Bureau of Statistics figures released on Tuesday show.

Lending to first home buyers fell 10 per cent and was down 29 per cent year on year, while investor lending fell 6.3 per cent in June but was up 17.3 per cent over the year.

Westpac senior economist Matthew Hassan said the impact of rising rates in an already cooling market had been rapid. Areas with higher property prices had been most sensitive to increases, but the slowdown in prices was spreading and the full impact had yet to be seen.

READMORE: New Cartier-inspired $159 million super yacht is a dazzling gem

House prices have pulled back by more than $100,000 in Sydney’s inner west, northern beaches and north shore. (Domain)

Hassan expects the cash rate to peak at 3.35 per cent in February, and property prices nationally to decline 16 per cent from peak to trough, with Sydney and Melbourne to see falls closer to 18 per cent. Hobart and regional areas that had unprecedented growth throughout the pandemic, partly based on temporary shifts in population, may also be in for a hard landing.

Hassan said most households had substantial savings buffers that would put them in good stead to handle higher mortgage repayments. However, it would be a delicate balance for the RBA to slow demand and inflation while not triggering widespread problems for the housing sector.

Raine & Horne Lower North Shore partner Alex Banning said prices were correcting after a period of enormous growth and markets that had higher price rises had further to fall.

“The RBA gave people false hope when they said rates weren’t going to go up until 2023, 2024, so a lot of people just out took big loans… we saw exponential growth.”

The market had swung from one extreme to the other, he said. While prices were lower, most buyers were still having to compromise due to their reduced borrowing power.

READMORE: Sydney’s own waterfront castle could be yours

Most households had savings that will allow them to manage higher mortgage repayments. (Domain)

Shore Financial senior credit advisor Greg Bishop was seeing more clients put plans to purchase on hold.

“No one really knows where the market is going to end up,” he said. “Prices have backed off … which is good for a lot of buyers, but they’re also facing increasing interest rates.”

Some lenders were honoring existing pre-approvals, Bishop said, as long as there was no critical credit change such as an increase in the loan to value ratio. Others were reducing borrowing capacity for pre-approved clients.

He urged those with pre-approval to check with their lender before purchasing a home as some buyers were finding out afterwards that their new borrowing power had fallen short.

This story first appeared on The Sydney Morning Herald

Mitsubishi says it has no plans to follow Honda and Mercedes-Benz with a fixed-price sales model in Australia, leaving room for customers to drive a bargain for the foreseeable future.

0

Mitsubishi Australia says it has no plans to switch to a non-negotiable fixed-price new-car sales model, as research shows most buyers prefer the ability to negotiate a good deal.

Fixed prices for new cars were introduced locally by rival Japanese brand Honda in July 2021, and German manufacturer Mercedes-Benz in January 2022.

Mitsubishi Australia CEO Shaun Westcott told Drive at this week’s 2022 Mitsubishi Outlander PHEV launch: “We have no immediate plans to change our (new-car sales) model in any way.

“We don’t have any preference for agency (the industry term for a fixed-price sales structure) and we haven’t got plans to go there at this point in time.

“I can’t say what the future holds because the world evolves, but we have no immediate plans and we’re not considering it.”

As previously reported by Drivethe Top 12 car companies in Australia say they have no plans to switch to a non-negotiable pricing structure.

The roll-out of fixed prices among a small number of car brands – which the industry refers to as an “agency” model because the dealers become selling agents under the new agreement, rather than owning the showroom stock – has been met with mixed success .

Sales of Mercedes-Benzes have increased since it went to the non-negotiable, fixed-price business model at the beginning of 2022, however Honda sales hit reverse since it made the switch in July 2021.

Supporters of the fixed-price approach say the new business model is designed to be fairer to customers who aren’t good negotiators.

However, detractors of the scheme say a fixed-pricing structure penalizes buyers who know how to drive a bargain, and limits the abilities of dealerships to offer sharp discounts – or generous trade-in valuations – to move metal.

Tom started out in the automotive industry by exploiting his photographic skills but quickly learned that journalists got the better end of the deal. He began with CarAdvice in 2014, left in 2017 to join Bauer Media titles including Wheels and WhichCar and subsequently returned to CarAdvice in early 2021 during its transition to Drive. As part of the Drive content team, Tom covers automotive news, car reviews, advice, and holds a special interest in long-form feature stories. He understands that every car buyer is unique and has varying requirements when it comes to buying a new car, but equally, there’s also a loyal subset of Drive audience that loves entertaining enthusiast content. Tom holds a deep respect for all things automotive no matter the model, priding himself on noticing the subtle things that make each car tick. Not a day goes by that he doesn’t learn something new in an everchanging industry, which is then imparted to the Drive reader base.

!['The reason why this is happening is awful. Everything else is meaningless, like how we are going to manage [without H&M],' a customer said. Pictured: A customer at the closing H&M in Moscow](https://i.dailymail.co.uk/1s/2022/08/04/00/61046467-11078935-_The_reason_why_this_is_happening_is_awful_Everything_else_is_me-a-99_1659568867448.jpg)