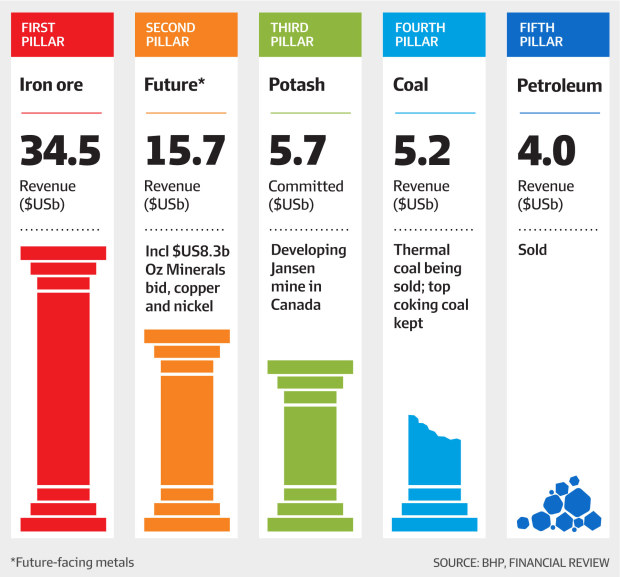

The dust on the massive Woodside deal only settled 74 days ago, but already Henry has steered BHP into another M&A maelstrom via an $8.3 billion bid for copper, gold and nickel producer OZ Minerals.

The offer was vigorously rejected this week by an OZ board that was convinced the $25 per share offer seriously undervalued the long-term opportunity that could come by combining the two companies’ copper mines in South Australia and nickel assets in Western Australia.

But few think the matter ended with that rejection.

“There are no sureties here, but you would think that [$25 bid] was the opening except for BHP if they were seriously considering OZ Minerals, which they obviously are,” said Blackmore Capital chief investment officer Marcus Bogdan.

Blackmore’s blended Australian equities fund owns both BHP and OZ shares.

Bogdan said he was pleased to see BHP acting opportunistically amid a slump in copper prices and the share prices of copper producers.

But he would be happy for BHP to spend more on a higher bid for OZ.

“I am not sure it needs a three in it [an offer priced above $30 per share] but it certainly needs to be materially above where it is today,” he said.

“We don’t have a definitive price on it, but it is certainly higher than the $25.”

‘Sharp focus’ on critical areas

Power is floating at the best of times and that was reinforced to Henry when he assumed the role of chief executive on January 1, 2020 and immediately had his first year in the job hijacked by the pandemic.

The word filtering out of BHP through 2020 was that Henry was frustrated by the situation; Melbourne’s strict lockdowns served as an apt metaphor for the way his plan to reinvent BHP had been put on hold by the immediate priority of managing a global workforce through a health crisis.

A disciple of thorough, data-driven process, Henry would buckle at the suggestion that an earthly emotion like frustration could influence strategy at a huge multinational like BHP.

But in February, Henry said the pandemic had left him with a “sharp focus on the critical few things, and getting them done super quickly.”

“As a big organization, too often we’ve failed into trying to do lots of things in parallel over a longer timeframe,” he said then.

“I’m a big believer that you should do fewer things, but get them done more quickly, then move on to the next few things.”

An extraordinary boom in iron ore and coking coal prices over the past three years has left BHP’s balance sheet in rude health, meaning Henry can move as quickly as he likes on deals.

Unification of the corporate structure also means BHP will find it easier to offer scrip when acquiring.

Two and a half years in, the Henry era is clearly about decarbonising BHP’s portfolio and gaining more exposure to the commodities that will thrive in a future focused on electrification and environmental sustainability.

Simplistically, the OZ bid is on-strategy because it would provide BHP with more copper and nickel; two metals that are expected to enjoy strong demand as the world urbanises, buys more household appliances and tries to decarbonise through electric vehicles, batteries and other means.

On closer inspection, it’s also about solving two problems; BHP doesn’t dig up enough nickel ore to run its Kalgoorlie nickel smelter at full capacity and buying OZ would give it extra volumes through the West Musgrave nickel, copper and cobalt project, which is ready to be turned into a mine costing more than $1 billion.

Aside from volume, West Musgrave’s ore contains the right balance of magnesium and iron that the Kalgoorlie smelter needs to run well; a chemistry conundrum that has increasingly occupied BHP’s nickel division in recent years as the profile of its ore has gradually changed through depletion.

Another effort to make Olympic Dam work

The other puzzle that BHP could solve by acquiring OZ – and the biggest motivation behind the deal – lies at South Australia’s Olympic Dam.

There are many reasons why Olympic Dam has been a difficult mine for BHP and delivered close to zero return on capital employed (ROCE) since it was obtained via the acquisition of Western Mining Corporation 17 years ago.

High uranium levels are the first challenge; state, federal and international governments have strict rules about the transport of radioactive materials such as uranium.

An aerial view of one of the Olympic Dam mines. AP

Olympic Dam’s high uranium content forces BHP to fully process the ore right through to the end of the energy-intensive process that makes red sheets of metal, about one square meter in size.

Most other copper miners, including OZ, have less uranium in their geology so can transport and export their copper as a gray concentrate that looks like soil.

OZ’s concentrate is an intermediate product and so requires far less processing; the Adelaide company’s customers do the smelting of the concentrate to turn it into pure metal.

Uranium is not the only challenge; the orebody at Olympic Dam is enormous but very deep underground and the copper occurs inconsistently throughout it, which is the opposite of what mining companies prefer.

Bringing the high-grade concentrate from OZ’s two nearby mines and blending it with the stuff BHP digs up at Olympic Dam would enable BHP to deliver a more consistent and predictable product into its smelter and refinery.

The blended product would also likely contain more copper than BHP sometimes puts into the system; the same volumes of a higher grade feedstock would derive more copper out the back end of Olympic Dam.

“Often times, when people think about growth, it’s all around growth in production. Now, growing production is a big lever, but really we should be thinking about growth as being growth in value, ”said Henry in February, when talking about his attitude from him to M&A.

‘Single point failures’

Other challenges at Olympic Dam are man made; Western Mining built infrastructure befitting a mid-tier miner.

BHP would have done it very differently if it had built the mine.

The mine design, where the capacity of the mine is roughly the same as the capacity of the refinery and the smelter, means that if one part of the system fails or underperforms, the whole system underperforms.

In that sense, Olympic Dam runs more like an integrated steel mill than a mine; there is “just in time” delivery from one part to the next unless it struggles.

Insiders refer to this as Olympic Dam’s series of “single point failures”.

If BHP had access to extra copper concentrate volumes from OZ, the smelter and refinery at Olympic Dam would be the bottleneck in the system; a much better scenario than the mine being the bottleneck.

BHP could fix Olympic Dam’s “single point failure” problem by building new mine shafts, concentrators, smelters and refineries, but it would be expensive; we can reasonably deduce that spending $8.3 billion buying OZ is the cheaper option.

There might also be productivity benefits at the two OZ mines – Prominent Hill and Carrapateena – if paired with Olympic Dam’s smelter and refinery.

OZ must mine selectively to avoid patches of ore that contain high levels of uranium because its regulators and customers won’t tolerate transportation of a concentrate with high uranium levels.

There have been numerous occasions in the past decade when a batch of ore from Prominent Hill was processed at Olympic Dam because it contained higher than normal levels of uranium.

Many believe uranium will become a bigger issue for OZ as its mines get older, the easiest bits of the resource have already been cherry-picked.

A full combination with BHP would reduce the need for Prominent Hill and Carrapateena to be mined selectively to avoid uranium, and that would probably deliver a productivity benefit and extend mine life.

OZ and BHP have talked on numerous occasions over the years about establishing a regular offtake agreement for OZ’s concentrate to be processed at Olympic Dam.

OZ has traditionally been reluctant to become too reliant on its big neighbor, and transactions have been sporadic.

If a merger can’t be struck, a deal for BHP to buy more of OZ’s concentrate could be a consolation prize.

“I think it makes strategic sense for BHP as it de-weights its exposure to iron ore and brings in a commodity that will become a more significant part of the portfolio,” says Bogdan.

“You want to be exposed to those metals that are going to be beneficiaries of decarbonisation and both copper and nickel form a key part of that.

“I think this transition that we are seeing is probably one of the most significant themes of the next decade.”