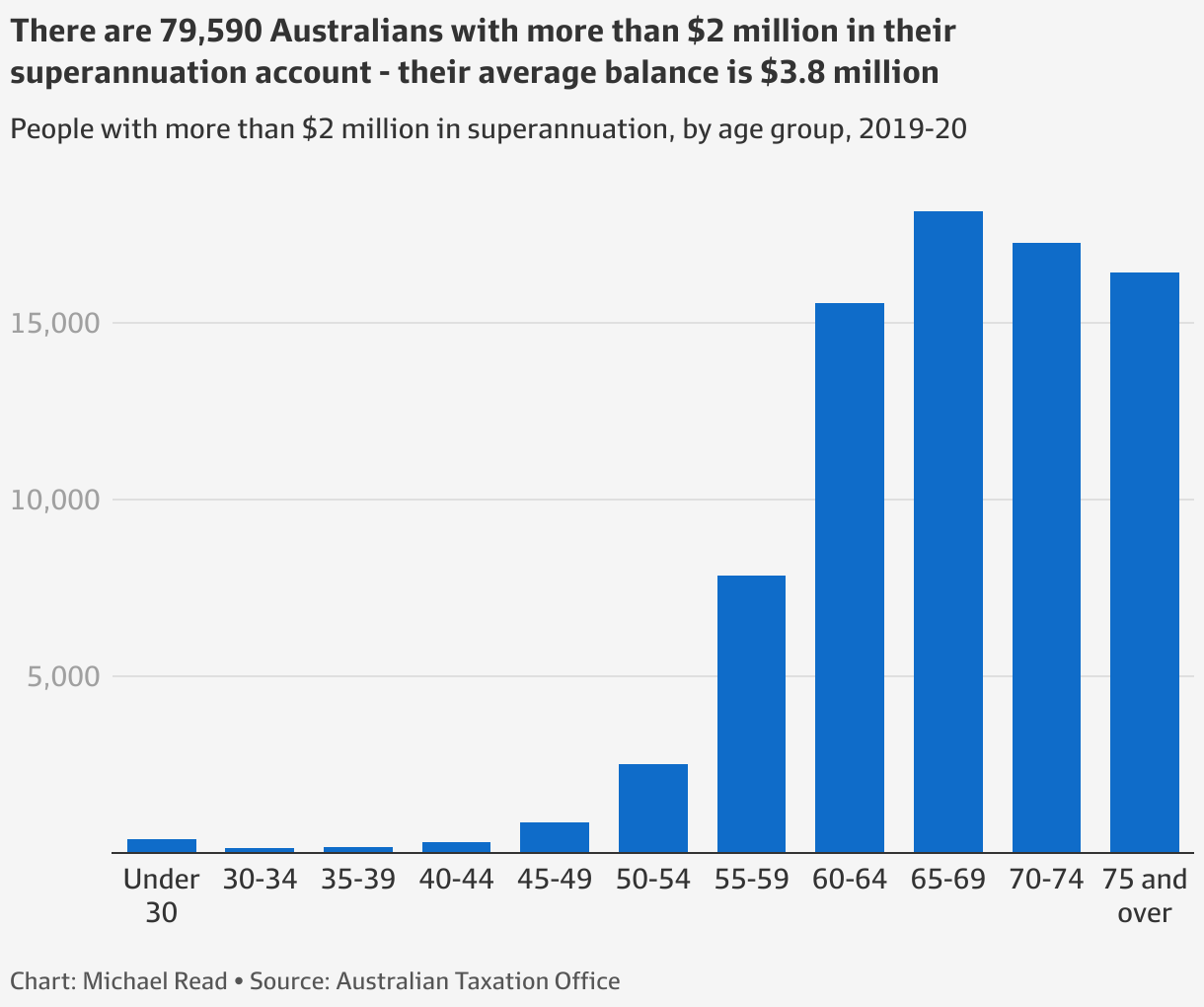

Among the cohort of wealthy savers with more than $2 million are 384 people aged under 30, who boast an average balance of $5.3 million. About 80 per cent of the young savers in this group either did not lodge a tax return or earned less than $18,200 in 2019-20.

Think tank the Grattan Institute estimates total earnings tax concessions for individuals with balances of $2 million or more were worth about $2.8 billion in 2019-20. The figure would have increased due to the strong growth in global equity markets following the early pandemic downturn.

The revelations have fueled calls among economists and influential super lobby groups for the Albanese government to reform superannuation tax concessions.

Independent economist Chris Richardson said the amount of concessions accruing to high-income earners was an “embarrassment” and called for a simpler system where superannuation earnings were taxed at a discount of 15 cents to a person’s marginal tax rate.

“So rather than starting with a flat tax and adding vast amounts of sticky tape and string, you start with a personal tax system and give a deduction for saving,” he told AFR Weekend.

Previous research by Mr Richardson found such a system would net the federal budget $6 billion per year, which would be enough to lower the company tax rate to 26 per cent from 30 per cent.

He said it would allow the tax office to do away with the complex system of contribution caps that govern how much money people can put into their super.

“Caps are God’s way of telling you the underlying system is wrong in the first place. You’re putting caps on because the incentives are wrong.”

Going beyond what’s needed

Super Consumers Australia director Xavier O’Halloran said there should be a threshold at which people no longer received a “leg up” from tax concessions.

“Superannuation, and the way it’s set up, is to incentivize consumers to save who wouldn’t otherwise to ensure they’ve got a good retirement.

“When we look at people who have managed to accumulate well beyond what might be needed to maintain the standard of living throughout retirement, we think it’s worth looking at whether the tax incentives are actually going beyond what’s needed to encourage [savings],” Mr O’Halloran said.

Richard Holden of the UNSW Business School said changes to superannuation rules should be considered, but only as part of a review of all aspects of the system.

“It would be much more sensitive to say that from now on all money that goes into super, and while it is in super, it is tax free. So all the compulsory contributions and voluntary contributions up to some amount are tax free, but we’ll tax it at the normal capital gains tax rate on the way out.

“Right now we have this weird thing where you tax it at 15 per cent on the way in, and you don’t tax it on the way out up to a cap, and it creates these awkward concerns about how much is enough?”

Professor Holden said reform of retirement subsidies could help address Australia’s structural budget deficit.

He said there were not that many $20 billion potential fixes but “retirement savings is one of them”.

Although Labor, before the election, said reform of tax concessions was not a priority, changes would help the cash-strapped federal budget and growing debt levels.

Wealthy savers are the main beneficiaries of federal government tax concessions.

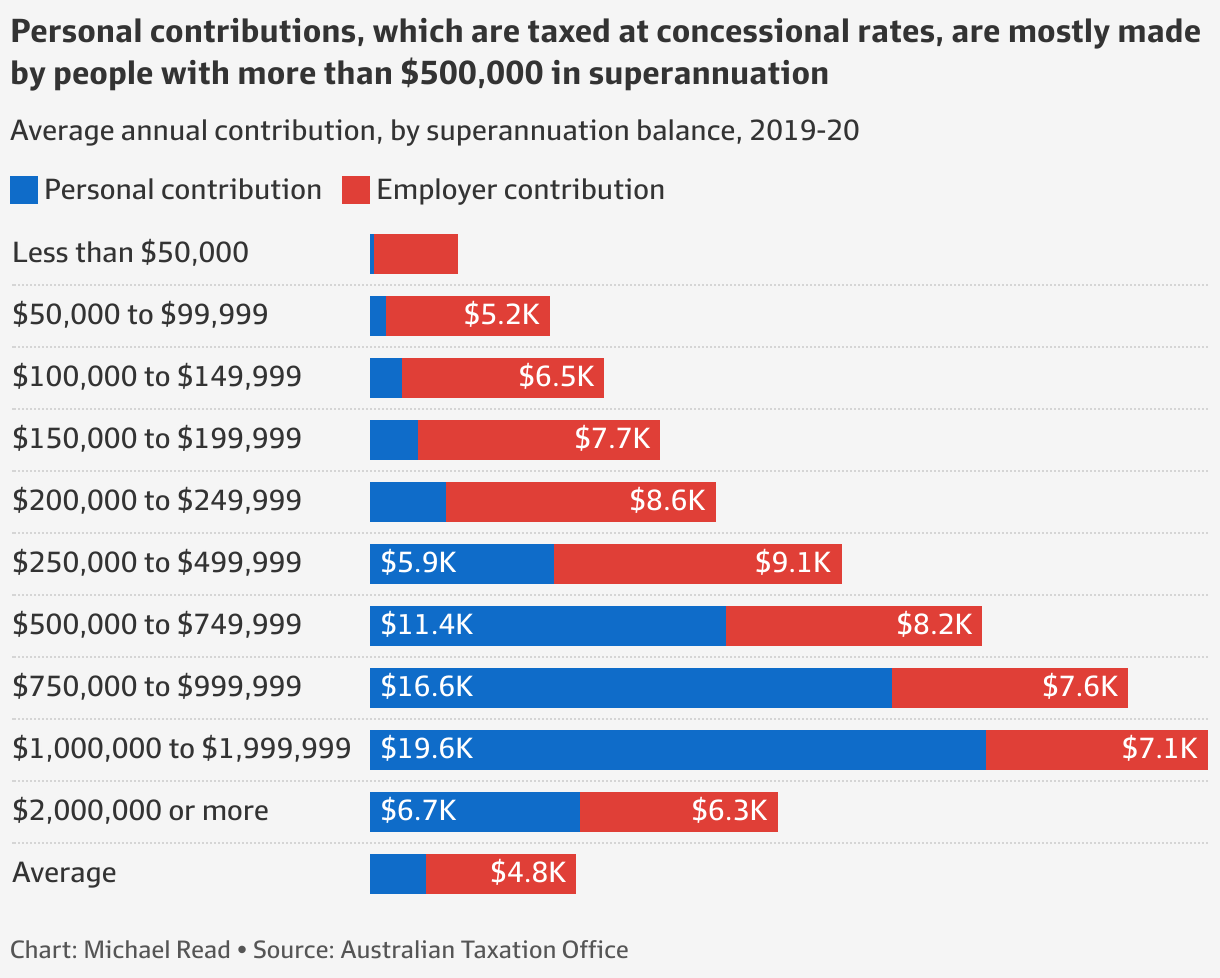

Just 6 per cent of people have more than $500,000 in superannuation, but they accounted for 48 per cent of the total value of personal superannuation contributions in 2019-20.

Personal superannuation contributions are taxed at the concessional rate of 15 per cent, up to an annual employer and individual contribution limit of $27,500. People who earn more than $250,000 pay an extra 15 per cent tax, but the additional impost still represents a hefty discount on the top marginal tax rate of 45 cents.

The average worker with more than $1 million in retirement savings made a personal contribution of $19,613 to their superannuation in 2019-20, compared to the $502 average top-up made by a person with a balance of between $50,000 and $99,999.

In the 2020-21 financial year, there were $19 billion and $1.3 billion in respective business and individual superannuation contribution tax concessions, according to the Treasury’s annual Tax Benchmarks and Variations Statement.

Combined, Treasury estimates that it is expected to amount to almost $93 billion over the next four years. Concessional taxation arrangements on super earnings cost the budget a further $10.6 billion in 2020-21 and are expected to cost almost $90 billion over the next four years. Individuals are generally taxed 15 per cent on their super earnings rather than their marginal tax rate.

Super cap calls

The Association of Superannuation Funds of Australia and the Australian Institute of Superannuation Trustees previously have called for balances to be capped at $5 million.

Grattan’s Joey Moloney and Brendan Coates said there was no justification for tax concessions for anyone with more than $2 million in super.

“At that level, people have more than enough for retirement and it looks more like tax-planning than anything else,” they said.

“This is particularly stark for those under 30 who already have $2 million in super, which has clearly come from contributions made by their parents.

“There is a strong case for capping total balances at around this level as such large balances are inconsistent with the primary goal of the super system of providing income in retirement.”

”These tax concessions are unsustainable with a structural budget deficit of 2 per cent of GDP. Treasury projects that by 2035, the total cost of super tax concessions will outweigh that of the age pension. Super tax concessions should be first against the wall to tackle the post-COVID budget challenge.“

UNSW taxation expert Bob Deutsch said current day and legacy tax concessions gave considerable scope for wealthy account holders to build their balances.

“Using the caps, you can over time put quite a lot of money into super. We’re not exactly paring it back at the moment.

“The downsizer super contribution rules have actually been increased so you can get more money in. I’m not surprised that there is a lot of money going into super.”

Professor Deutsch said concessions were an appropriate way to encourage proper saving for retirement, but changes could be required.

“The problem is that superannuation funds have become used now for broadly more wealth creation purposes. I don’t think that was ever really the intention.”

“It was not meant to be money pot that could just grow to provide people with wealth. It was more meant to be about giving them sufficient funds to enable them to have a reasonable retirement, without having to lean on the public purse.”

He said changes to the rules could be politically tricky for Labor, but reforms by the former Coalition government did have an impact.

“You’d want to be very careful about how you limit access to super, because you don’t want to ruin it for people who are using it generally build a retirement lump sum,” he said.

Greens spokesman Nick McKim said anyone with $2 million in their super “doesn’t need tax concessions beyond the [$1.7 million] balance cap”.

“We stand ready to work with the new government to make super fairer,” he said.

“We should get rid of tax breaks for the super wealthy which are basically publicly subsidized estate planning. This is low-hanging fruit.”

“The recent retirement income review found that the richest 10 per cent get more public subsidies than anyone else. This is a corruption of what superannuation was designed to be, and it needs to end.”