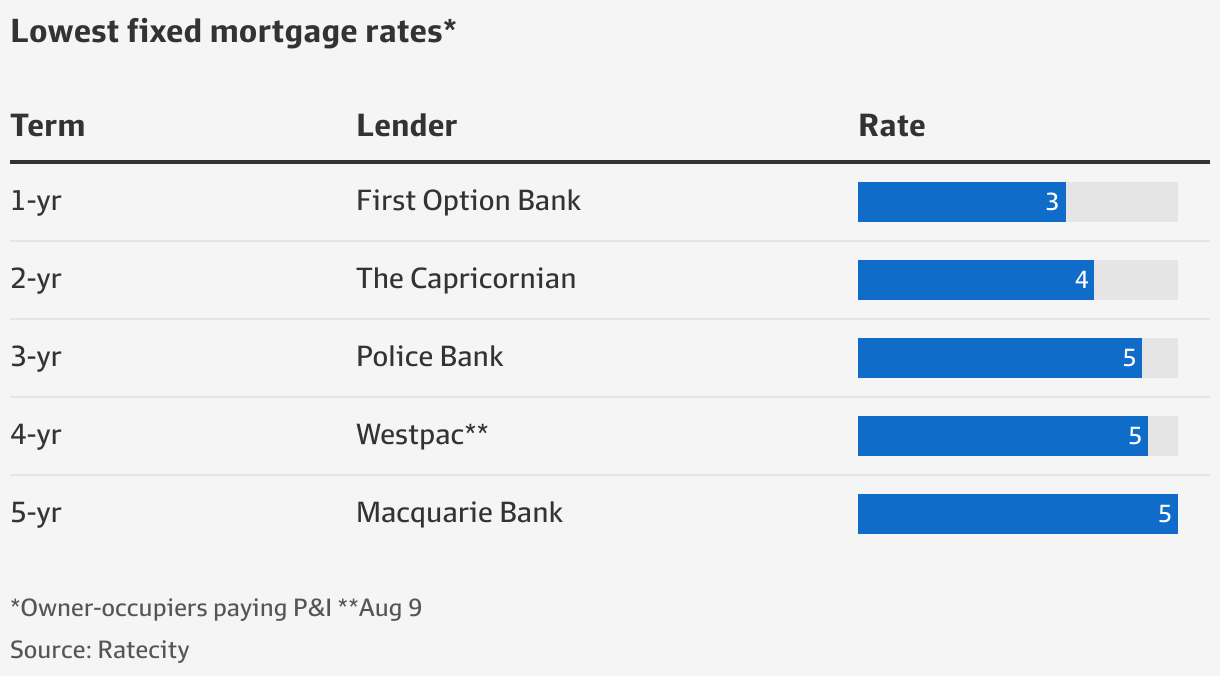

Westpac’s rate falls to 4.89 per cent for borrowers with a 30 per cent deposit.

Mortgage brokers said the new fixed rates could be “very, very attractive” to borrowers seeking a lower-cost product – even if it was more than double the average fixed rate on offer two years ago – particularly if variable rates rose.

They expect other major lenders to offer competing fixed-rate products with lower rates and shorter terms.

Expect a lot of activity

“Those cheap loans will start to roll off in volume by the end of this year. A lot of property buyers will be looking for a new loan or to roll over their existing loan,” said Brendan Coates, an economist at the Grattan Institute.

“There’s likely to be a lot of activity with borrowers looking for new loans because they will be coming off a low fixed rate to a much higher variable rate.”

Despite the push by banks to offer a “cheaper” fixed-rate alternative to variable rate loans, many borrowers whose mortgages are set to expire in coming months will face significant increases in their repayments.

More than 90 per cent of fixed-rate borrowers whose loans expire in the next 18 months will face an increase in repayments. That rise will be as high as 20 per cent for about half of them.

Major broker groups, such as ASX-listed Australian Finance Group, say the number of borrowers fixing rates has fallen from highs of nearly 40 per cent during COVID-19 to less than 8 per cent as banks priced in rate rises.

AMP chief economist Shane Oliver said: “Lower bank longer-term fixed rates relative to their variable rates make sense because bond yields have failed since their peak in June.”

Rates for fixed-term mortgages reflect what is happening in the bond market, which is where banks, companies and governments borrow money.

For example, since June, the four-year bond yield has failed from just below 4 per cent to below 3 per cent.

Variable rates are determined by the RBA’s cash rate, which is still rising. On Tuesday, the RBA pushed rates up 0.5 of a percentage point to 1.85 per cent.

“The decline in longer-term bond yields reflects bond investors’ perceptions that slowing growth and recession is now a rising risk and that inflation will fall after peaking later this year,” Dr Oliver said.

“That in turn will see the RBA’s cash rate peak at levels lower than expected and maybe earlier.”

Sam White, executive chairman of the Loan Market Group, a leading mortgage broker aggregator, said: “The cut in four-year rates reflects that the medium-term outlook for rates is not as dire as short-term predictions. The fixed rates seem to reflect an expectation that while there will be more short-term rate rises, these will be moderate.”

Sally Tindall, research director of RateCity, which monitors fees and rates, said the cheapest variable rates from the big four were 3.77 per cent, which is 113 basis points lower than Westpac’s four-year rate. But cash rates are expected to increase by another 1.5 percentage points, or 150 basis points.

Mortgage brokers say the lower fixed rates will begin to look increasingly attractive as variable rates rise.

Phoebe Blamey, director of Clover Financial Solutions, said: “There’s going to be a bucket full of borrowers coming off a fixed rate looking for a fixed rate cheaper than variable.

“This will become a very competitive part of the market.”