What SolGold does have is a large and promising copper/gold/silver project in Ecuador, called Cascabel, that it is trying to develop at a $US2.7 billion ($3.8 billion) pre-production cost this decade.

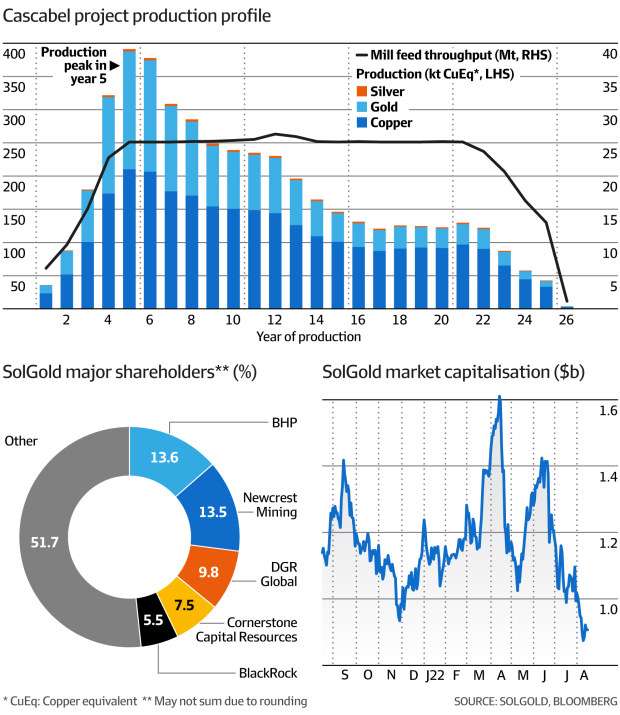

If all goes to plan, SolGold reckons it could mine Cascabel for 26 years at 210,000 tonnes of copper equivalent a year (about the same as BHP’s Olympic Dam mine), and generate $US14.4 billion cash flows after tax, based on copper at $US3.60 to pound. (At recent spot prices, it would be $US16.3 billion in after tax cash flows, according to SolGold’s presentation to fund managers dated last month.)

SolGold owns 85 per cent of the Cascabel project.

While SolGold couldn’t raise equity at the drop of a hat last month, it’s not because it doesn’t have deep-pocketed backers. Remove the contrary.

SolGold’s two biggest shareholders are Australia’s BHP and Newcrest Mining, with toehold stakes worth 13.6 per cent and 13.5 per cent of the company, respectively.

With SolGold reported to have only enough cash to see it through to the end of the year (after scrapping its recent $50 million top-up), there’s bound to be a time in the next few months when its two big Australian shareholders will have to decide how much they want Cascabel.

If it’s a bit, then the two shareholders will have to tip into an equity raising and try to maintain the status quo.

But if it is a lot, like some analysts suspect, then we could see a pair of Australian heavyweights in a ding-dong battle.

The company’s annual general meeting, slated for November, is a key date to watch.