An Aussie home owner has shared a very simple hack that promises to significantly reduce the drying time of your laundry this winter.

Sharing on a popular Facebook group, the woman revealed how one easy act – which takes just five seconds to do – can leave your damp clothes dry and ready to be folded in no time.

She said the hack was perfect for anyone who dries their laundry inside the home in front of a heater or fan.

For more Lifestyle related news and videos check out Lifestyle >>

The Facebook user starts by hanging the wet clothes on a drying rack as usual and placing it a safe distance from the heat source.

She then suggests hanging a larger piece of clothing on the far end of the airer – the side that’s opposite the heater of fan.

The action effectively blocks the hot air in and keeps it circulating around the laundry, drying the clothes quicker.

In her post, the home owner said it was a great way to dry your laundry without wasting electricity a clothes dryer.

By hanging a large piece of clothing at the far end of the clothes rack, it traps in the heat and dries your clothes faster. Credit: Cleaning & Organizing Inspiration Australia/Facebook

“To help if you dry clothes near heater, turn sideways and block other end with larger piece, adjusting as needed,” she told the Cleaning & Organizing Inspiration Australia Facebook page.

“The heat doesn’t blow through as quickly, so the clothes dry faster and you stay warm without guilt!”

Many Facebook users were blown away by the easy hack.

“This is mega inspiring!” said one.

Added another: “Simple but effective. Have just bought a clothes horse to save on the dryer.”

‘Instant dryer’

Write a third: “Drying clothes, staying warm, and saving money and resources. Just like our grannies did!”

Others had a few twists on the simple tip to speed up drying time even more.

“Wrap a sheet around three sides and the top. Instant dryer,” said one.

Another added: “Yes I second this! I find putting something on top works well too.”

Added one more: “I used to put a sheet over the lot to keep the heat in and dry them quicker, especially if you can put them over a heating duct.”

Safety warning: Clothes should always be placed more than a meter from any heater or fan.

Passengers crawl into baggage carousel hatch to grab suitcases after delays

Passengers crawl into baggage carousel hatch to grab suitcases after delays

Instead, the Bank of England’s announcements are being seen so far as refreshingly direct and honest. They are also acting as a catalyst for serious discussions and analysis and, as important, deeper consideration of what is being proposed by the two candidates for prime minister.

‘Trusted adviser’

The Bank of England is reminding the world what a politically independent central bank can and should do: act as a “trusted adviser”, willing to share analytically honest views that other more politically sensitive institutions are either unable or unwilling to do.

Of course, this is not a risk-free approach. Such honesty – rather than catalyzing appropriate responses from policymaking agencies that lead to better economic and social outcomes – can provoke household and corporate behaviors that accelerate the bad outcomes.

Yet the risks involved are worth taking, especially when the alternative is a central bank that loses institutional credibility, sees the effectiveness of its forward policy guidance erode and becomes even more vulnerable to political interference.

It should also be noted that the UK’s situation differs in some important way from those of other countries. The country’s economic challenges are complicated not only by the energy price catch-up but also by the political transition and the changing nature of the country’s relations with its trading partners.

This is not to say that the implications for other countries do not go beyond the importance of analytical directness and intellectual honesty. They do. Indeed, I can think of four others:

Illustrating the elusiveness of “first best” policy responses in a world in which central banks fell behind in responding to inflation. Acting as a reminder that, in such a world, the prospects of high inflation and recession can coexist.

Highlighting the need for central banks to act relatively aggressively despite the likelihood of inflation destroying demand. Stressing the need for governments and multilateral institutions to assist in efforts to contain inflation, promote productivity and growth, and protect the most vulnerable segments of the population.

I suspect that, in the next few days, the Bank of England will again discover that it is not easy to be the messenger of unpleasant news, no matter how honest and well-intended the approach is. Yet the example it sets for other central banks is an inspiring one, as is the possibility of acting as a catalyst for a more holistic response to the UK’s economic and social challenges.

Mohamed A. El-Erian is a former chief executive officer of Pimco, he is president of Queens’ College, Cambridge; chief economic adviser at Allianz SE; and chair of Gramercy Fund Management.

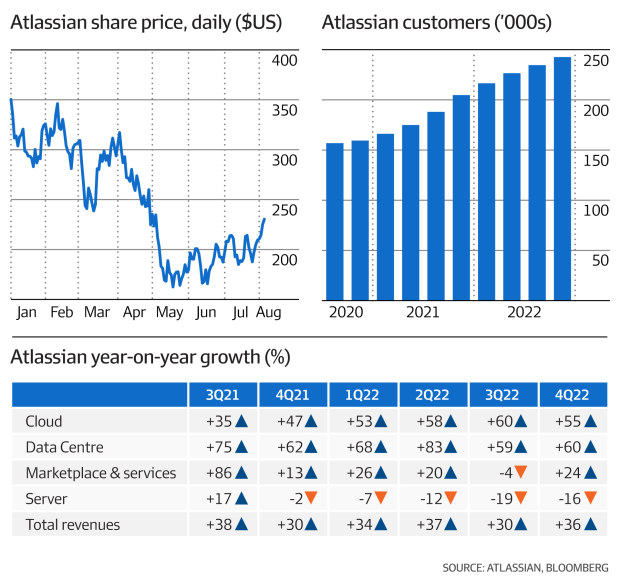

The company ended the 2022 fiscal year with roughly the same amount of free cash flow as the previous year, of $US763.8 million.

In a shareholder letter, co-chief executives Scott Farquhar and Mike Cannon-Brookes said they had hired 634 new employees in the quarter, mostly in research and development roles and over 2,300 new staff members in the 2022 fiscal year.

Co-CEO and founder Mike Cannon-Brookes. Atlassian doesn’t expect to lose customers as companies cut costs. Oscar Coleman

“We firmly believe that Atlassian is uniquely positioned, having deep-seated momentum and a differentiated business model. This gives us the confidence to make incremental investments – despite the current environment,” the CEOs wrote.

“That will fuel even more durable growth over the long term and deepen our strategic advantages. We know this is an unconventional choice right now and want to be open with our investors about it.”

Atlassian’s bosses believe it is somewhat insulated from tightening economic conditions as its products are targeted at technology developers, who they say are typically the last roles businesses cut back when they are tightening their belts, especially with many companies working on digital transformation plans.

“While our products punch above their weight in terms of value, Atlassian is a relatively small line item in overall IT budgets and likely not where customers look to reduce costs,” the CEOs said.

New CFO

The company has flagged “line of sight” to $US10 billion in annual revenue and has a new executive in charge of marshalling the numbers in former Microsoft finance president Joe Binz, who will become chief financial officer in September.

Mr Farquhar had acted as an interim CFO for the current earnings period.

The company said Mr Binz was responsible for Microsoft’s financial planning and analysis, investor relations, acquisition integration, and procurement functions across a 20-year stint at the tech giant.

It is the second earnings call in a row where Atlassian has unveiled a new senior executive hire, having announced Rajeev Rajan as his chief technology officer – hired from Facebook parent Meta – in April.

In guidance for the next quarter, Atlassian forecast revenue in the range of $US795 million to $US810 million, and a widening loss per share of $US1.17 to $US1.16 – compared to a loss of $US0.41 in the fourth quarter.

“We believe our investments will propel us past this [$US10 billion revenue] milestone faster, while further strengthening our strategic position,” the CEOs said.

“History shows that turbulent economic environments offer a chance for companies to gain market share – to shake up the leaderboard. Atlassian intends to seize this moment.”

‘tech wreck’

With reference to the broader “tech wreck” that is seeing job losses and valuation mark-downs at tech companies around the globe, the co-founders reiterated remarks made by Scott Farquhar earlier this year about the current downturn and potential recession not being Atlassian’s “ first rodeo.”

“We seized opportunities during the economic turbulence of 2008-2009 to scoop up talent that wouldn’t have been available otherwise and broadened our customer base by offering $10 starter licenses for our products,” they wrote.

“Today we’re echoing that approach with free editions of our cloud products and ambitions to more than double our headcount over the next few years. Playing offense when others were throwing off their back foot worked for us then, and we’re confident it will work for us now.

From a commercial perspective, Atlassian said the ongoing transition of customers to its cloud-based products was continuing well, with a focus on driving a growth rate on sales of third-party cloud apps on its marketplace, greater than that of its own products.

It said it closed the financial year with over 200,000 cloud customers and cloud revenue growth in the fourth quarter of 55 per cent year-over-year.

Atlassian also confirmed that its parent holding company would shift from the United Kingdom to be domiciled in the United States, pending shareholder approval at two special shareholder meetings to be held on August 22. If shareholders agree the company will become based, as well as listed in the US from September 30.

“We believe moving our parent entity to the United States will increase our access to a broader set of investors, support inclusion in additional stock indices, improve financial reporting comparability with our industry peers, streamline our corporate structure, and provide more flexibility in accessing capital. ,” the co-CEOs wrote.

Regarding The Oaks and other big-ticket hotel offerings, Musca says these properties and businesses have benefited from decades of planning, licensing, gaming and capacity approvals in premier locations that would be almost impossible to replicate as new developments.

“Fundamentally the very best hotels in the premier locations are simply going to enjoy perpetual, unimpeded earnings growth without competition.”

$175m would set a record

Stuart Laundy, son of billionaire pub owner and Rich Lister Arthur Laundy, confirmed his family would be among those looking closely at The Oaks as a potential acquisition opportunity.

He said he couldn’t comment on whether it was worth $175 million as he had “no idea” yet of its turnover or other performance figures but said, “if someone paid $175 million tomorrow, it would not surprise me”.

“Pubs are a safe option. People have always enjoyed a drink and had a punt, it’s not a bad business to be in. Even during the Great Depression, pubs were still pouring beers,” he told AFR Weekend.

The Oaks is best known for its beer garden.

Whether The Oaks is worth as much as selling agent JLL is quoting will be determined by the market – should it fetch $175 million it would set a land rate record across both residential and commercial property on the Lower North Shore.

Generating about $23 million in annual revenue, The Oaks comes with multiple bars, including Taffy’s Sports Bar, the Bar & Grill restaurant, a gaming room with 30 poker machines, extensive first floor function spaces and high-end retail bottle shop. There’s also the potential for a five-storey development.

The Crossroads Hotel sold with 30 electronic gaming machines that bring in over $300,000 a week, a restaurant serving over 4000 meals a week and a large accommodation component across a 1.28-hectare site, six times as big as The Oaks.

“Assets such as Crossroads Hotel and Strathfield Hotel are frankly inimitable, and have separately enjoyed robust earnings platforms for decades,” said HTL Property’s Andrew Jolliffe, who brokered the record sale of both properties.

That does not mean the sector is immune to a crash, as occurred during the global financial crisis, when a mountain of debt brought down big pub giants like National Leisure and Gaming and the Hedley Group.

However, this time around owners are far less leveraged and good operators are generating healthy operating margins exceeding 20 per cent.

“When compared to other periods, loan-to-values are actually at an industry low point, with the average sitting below 50 per cent. Accordingly, the capitalization of Australian pubs has rarely been more balanced,” says Jolliffe.

Private equity firm Adamantem Capital has locked in a deal to buy KKR-backed GenesisCare’s cardiology business, CardiologyCo, after about six weeks of exclusive talks.

GenesisCare CEO Dan Collins had Record Point and Morgan Stanley running the auction for his cardiology care business, CardiologyCo. James Alcock

Adamantem is understood to have paid between $200 million and $250 million. It would own the lion’s share of the CardiologyCo, while the doctors would keep a minority shareholding, under a deal that was signed this morning.

It gives the PE firm exposure to the aging thematic, while CardiologyCo gets to lighten its debt load.

CardiologyCo has more than 100 cardiologists and 700 odd technicians who see 200,000 plus patients a year. It would make two bolt-on acquisitions and expand into Sydney and diagnostics, concurrent to the Admantem deal.

Adamantem dealmakers Angus Stuart, Gunjan Goel and Georgina Varley led the investment for the firm. It joins its other healthcare bets like Zenitas and NZ aged care business Heritage Lifecare. It is the fourth investment in Adamantem’s $800 million Fund II after Climate Friendly, Linen Services and Nak Hair.

The PE firm used Grant Samuel, Skye Capital, EY and Gilbert + Tobin for advice. GenesisCare was advised by Record Point, Morgan Stanley, PwC and Herbert Smith Freehills.

“The cost-of-living crisis, and now the rapid and brutal hike in interest rates, is forcing many workers to deplete their savings. They simply cannot withstand their wages continuing to go backwards in real terms.”

Treasurer Jim Chalmers said Friday’s RBA statement reinforced the “significant challenges” Australian households were facing, including higher interest rates, rising costs of living and falling real wages.

“Our economic plan is a direct and deliberate response to the challenges facing our economy,” he said. “That’s why we are working hard on responsible cost-of-living relief, easing capacity constraints and increasing productivity in the long run.”

Shadow treasurer Angus Taylor said the RBA’s statement showed Chalmers was “already at odds” with the bank, just a week after delivering his own economic statement to parliament.

“Not only did the treasurer fail to deliver a plan, his forecasts were out of date within a week,” he said.

loading

The latest RBA forecasts are a significant downgrade from its previous monetary policy statement in May, when the RBA was expecting household income to grow by 0.9 per cent in the final three months of this year. Now it believes it will shrink by 0.9 per cent.

The bank said people would soon start to feel the impact on their home budgets, admitting those dependent on welfare payments could struggle as a larger proportion of their income went to necessities that are rising in price including food and fuel.

“While household balance sheets are generally strong and many households should be able to absorb these price increases, others have limited savings buffers and may have to reduce spending elsewhere,” the report said.

“For some of these more vulnerable households, the impact of price rises will be mitigated to some extent by the indexation of social assistance payments twice per year, though price rises will reduce recipients’ real incomes in the near term.”

The RBA downgraded all its forecasts for economic growth over the next two years. By December this year, it expects GDP to be expanding at an annual rate of 3.2 per cent, compared to its 4.2 per cent forecast made three months ago.

By the middle of 2024, economic growth is tipped to be down to 1.8 per cent.

Wages growth, while picking up, is not expected to accelerate much above what the bank had been forecasting. It expects the wage price index to be climbing by 3.4 per cent in mid-2023 and 3.8 per cent in mid-2024.

Consumer prices, despite the RBA’s lift in interest rates, are also tipped to grow strongly.

Inflation is expected to peak at 7.8 per cent in the December quarter, edge down to 6.2 per cent by the middle of next year and still be at 3.5 per cent in the June quarter of 2024.

loading

Unemployment, however, is expected to defy the tightening in monetary policy. It is forecast to be at 3.4 per cent by the middle of next year and inch up to 3.7 per cent 12 months later.

Commonwealth Bank’s head of Australian economics, Gareth Aird, said the forecasts were not good news for Australian households.

“We believe that high inflation coupled with aggressive rate hikes and falling home prices will be the more dominant force on household consumption from here,” he said.

In response to inflationary pressure, the RBA has lifted interest rates by 1.75 percentage points over four consecutive months this year, its most aggressive increase in rates in nearly 30 years.

The RBA said the “competing forces” of a tight labor market, which leads to stronger wage growth, and increasing cost-of-living pressures made predicting household spending “unusually uncertain”.

“Employment growth could be stronger than expected, and strong household balance sheet positions could support household consumption by more than anticipated,” the report said.

“Alternatively, a decline in real incomes for the average household could weigh on spending more than expected, particularly if household wealth is also declining.”

All major economies are facing increasing headwinds caused by the sharp lift in global inflation, supply chain disruptions and strong domestic demand.

Harvey says he has recently increased rentals on a portfolio of properties in Sydney and Brisbane by about 10 per cent.

“Many investors are sitting and waiting [to get into the market]but smart ones realize the time to move is at the bottom of the consumer sentiment curve to benefit from rising yields throughout the correction phase,” he says.

Rental increases

According to CoreLogic, which monitors property market prices, rents have increased more than 30 per cent across inner Melbourne over the past 12 months, despite little demand pressure from immigration.

Research director Tim Lawless says rents are set to continue increasing as demand outpaces supply.

According to analysis by SQM Research, which monitors property markets, total residential vacancy rates are at a record low of about 1 per cent, or less than half of vacancy levels during the past 15 years.

But SQM’s managing director, Louis Christopher, says there are signs of a peak in the rental market in regional Australia, with a larger number of regions recording rising rental vacancy rates and some falls in rent.

Investment bank Morgan Stanley says house prices fell at their fastest rate in nearly 40 years during July as rate rises increased pressure on credit availability and borrowers’ capacity to service loans.

Prices are about 2.6 per cent below peak levels, with falls led by Sydney, Melbourne and Brisbane.

The bank predicts cash rates, which have increased over each of the past four successive months, will continue to rise from 1.85 per cent to 3.1 per cent by the end of the year.

“We expect a national decline in house prices of 10 per cent possibly by the end of the year if the current rate of decline holds, with next year also likely to provide only limited relief,” the bank said.

National house price falls, which accelerated during July, are expected to total about 15 per cent, it predicts.

Planned auctions for this weekend are more than 20 per cent down on last week and 5 per cent lower than the same time last year, according to CoreLogic.

Buying on the dip

Chris Foster-Ramsay, principal of Foster Ramsay Finance, a mortgage broker, says many property investors have been sitting on cash waiting for a market downturn because they are confident the market will rebound.

“They are buying on the dip,” Foster-Ramsay says. “The market came back in the past and investors are confident it will happen in the future, particularly as immigration begins to increase.”

In Perth, Karen Firth, director of Art of Real Estate, says: “Investors are back and looking for properties within a 10-kilometre radius of Perth.”

Melbourne buyer’s agent Cate Bakos says there has been a rapid switch in buyers from owner-occupiers to investors attracted by low vacancy rates and the prospect of consistent rental returns, a cash flow boost and diversifying investment portfolios. They are typically looking at inner-urban areas or within a two-hour drive of the central business district, she says.

About 30 lenders are attempting to attract new investors with cashback offers, an upfront incentive to cover switching costs, according to analysis by RateCity, which monitors fees and costs.

The highest cashback is $10,000 for loans of more than $2 million from Reduce Loans, which charges higher rates for cashback deals, says RateCity.

The highest for $1 million is $6000 from Citi, available only through mortgage brokers.

The accompanying tables show the most competitive investor mortgage rates for interest-only and principal-and-interest loans. Investors considering cashback offers should use these as a guide to negotiating lower rates and bigger discounts.

Many investors are attracted by rising gross yields as property prices fall and rents rise.

Gross yield is calculated by dividing the annual income from the property by its sale price.

National gross unit yields rose six basis points to about 3.9 per cent in June – and 26 basis points year-on-year – as rental growth outpaced capital gains. Yields in Perth are about 5.5 per cent, Melbourne 3.7 per cent and Sydney 3.3 per cent, according to CoreLogic.

But gross yields do not reflect continuing costs associated with property investments, such as strata levies, rates, repairs, maintenance and myriad taxes, including state-based land tax.

Aldi Australia has made a major change to its online store, leaving customers disappointed.

Last year, Aldi announced a trial where shoppers could purchase some of its Special Buys items online, but it has now been revealed it has concluded.

In discussing the change, a spokesperson for the German supermarket chain said while the trial provided valuable insight and some customers enjoyed the online ordering option, it “wasn’t the right time to expand”, 7 Life reported.

“Supply chain pressures and inflation means that our top focus [is] to deliver the best priced groceries to Australians. We believe that this focus, while it might come at the cost of other projects, delivers the best value to our customers,” the spokesperson said.

“We have been clear that delivering quality groceries at the best prices is our ongoing goal, especially when we are seeing Australians feel the pressure of inflation.

“Our unique business model is built on efficiency, and while we don’t want to see customers disappointed, we believe this is the best decision to continue maintaining our price gap of over 15 per cent compared to our competitors.”

The spokesperson said there was no immediate plan to bring online Special Buys back but Aldi wouldn’t rule it out for the future.

News.com.au has contacted Aldi for further comment.

Aldi first announced alcohol and Special Buys would be available online early last year, with plans to eventually have the store’s entire range online.

At the time of the announcement, Aldi CEO Tom Daunt, said groceries could be added at a later date but e-commerce was set to be part of the supermarket’s future as the Covid-19 pandemic accelerated Aussies’ online shopping habits.

Aldi customers were quick to spot the backflip by the supermarket.

“So did Aldi just quietly remove their online range instead of the promised expansion of eventually offering all their products online?” one person asked on social media.

“I can’t see any mention of online products anymore anywhere on their app or website ever since they had their online clearance last week.

“And they used to offer all the larger items like the table saw for delivery, but not any longer.

“I really feel like they’re removing the option altogether.”

Others noted that clearance items were still on offer online.

The anger in Australia over the behavior of the natural gas cartel, described in infuriating detail this week by the ACCC, is another symptom of the growing global disillusionment with free markets.

The global energy crisis caused by the Russian invasion of Ukraine on top of the growing evidence of the impact of global warming is leading to more and more calls for much greater government intervention.

In Europe, where gas prices have already increased 52 per cent with more certain rises, politicians are under pressure to find solutions that the market is unable to provide.

This week I spoke to Kevin Bailey, Australian chairman of a small locally listed company called Po Valley Energy, which own gas fields in the north of Italy and the Adriatic Sea. After years of fighting environmentalists and the Italian bureaucracy to start producing gas, suddenly the government in Italy, egged on by Germany, is falling over itself to help Bailey get production going.

In Australia, the ACCC’s gas inquiry interim report is a devastating critique of what happens when a private cartel gets control of an essential product, any product for that matter.

ACCC chair Gina Cass-Gottlieb is calling on the federal government to trigger what’s called the Australian Domestic Gas Security Mechanism (ADGSM), having found that the five LNG exporters that control 90 per cent of Australia’s gas will leave Australians 56 petajoules short next year, while at the same time enjoying a huge lift in profit margins as a result of a crippling rise in gas prices.

The context for Australia’s struggle with the gas cartel is global, and wider than energy: The war in Ukraine has once again exposed frailties in the global economy caused by the rolling back of government regulation over the past 40 years.

The dangers of weak regulation

The first demonstration of this was the GFC, when the world’s private banks came unglued and would have brought down the global economy entirely if it hadn’t been for massive state intervention and fiscal support.

That led to some extra regulation of banks, but no broader reordering of priorities or fundamental change in the philosophy of governing, and now the world’s private energy firms are at it.

One thing that did happen as a result of the GFC was that central banks became completely unconstrained.

They had been given independence a decade or more before that, but after 2008 they started generating “free money” through quantitative easing.

Governments that were weighed down by huge deficits as a result of the banks’ self-destruction in 2008 were only too happy to let their own central banks take the running and print trillions of dollars to keep economic growth going in the absence of either fiscal support or productivity growth.

The result is that most economies now require $US3-$US5 of debt for every incremental dollar of GDP, versus $US1.50 in the 1950s, ’60s and ’70s. Overall global debt has grown to 350 per cent of GDP, from 152 per cent in 1990.

Today’s total freedom of central banks to adjust interest rates and print money is actually another expression of the distrust of politicians that began with Friedrich Hayek and Milton Friedman, and led to 40 years of trust in free markets and private ownership, along with lower taxation.

In a way, central bank freedom to create money has replaced the spending of tax-cutting, deficit-burdened governments, except that rather than support the welfare state and better government services, it has pushed up asset prices and benefitted the already rich.

As discussed in this column a couple of weeks ago, it’s hard to work out whether tax cuts have been ideologically designed to curtail the size of the state, or are simply the greed of plutocrats wanting to cut their own taxes, but lower taxes is definitely what happened, especially at the highest-income tax brackets:

AUSTRALIAN TOP MARGINAL INCOME TAX RATE

Source: Australian Treasury

eroding social cohesion

Australia’s top marginal rate is now 45 per cent (plus a Medicare levy of 2 per cent), and while that is set to remain when the Stage 3 tax cuts are implemented in 2024, the income at which it cuts in will be increased to $200,000 , and the 37 per cent tax rate is to be removed entirely so that most people will pay a flat income tax of 30 per cent, making the tax system much more regressive.

Taxes have become steadily less progressive, more regressive around the world over the past 40 years, dramatically worsening inequality.

Research by Thomas Piketty for his book A Brief History of Equality shows that in the US, the top 1 per cent have gone from 9 per cent of total income in 1970 to 22 per cent today, while the share of the bottom 50 per cent has gone from 21.2 per cent to 13.2 per cent. No wonder they’re not happy.

All governments now face two great challenges, one easier than the other: First, how to re-engage in the regulation of private firms and even nationalisation, and second, how to pay for the expansion of the state that is now demanded.

Continuing to rely on central banks to support growth by printing money, while constraining taxes and government spending, is clearly not viable because of what that does to inequality and social cohesion.

Viktor Shvets of Macquarie Research in New York believes that central bank independence will not survive: “…rather central banks will be probably rolled back into departments of finance and treasury, where most of them belonged back in the 1950s-’60s”.

He wrote recently: “It is a question of choosing between two evils: Pursuing hyper-aggressive monetary policies coupled with regressive taxes, [which] will likely cause even greater polarisation, social, political, and geopolitical dislocations, [or] altering today’s policies, [which] is not only hard but also risks “throwing [out] the baby with [the] bathwater.”

Shvets may be right, but in the meantime the simpler solution in this country at least is to abandon the Stage 3 tax cuts and to prepare Australians for higher taxes and a larger, more hands-on government.

Climate change and the prospect of a long, drawn-out conflict in Ukraine will mean there is no alternative: The private sector cannot sort those things out.

Catastrophe and war are matters for government.

Alan Kohler writes twice a week for TheNewDaily. He is also editor in chief of Eureka Reportand finance presenter on ABC news