Mr Di Sibio told the Financial Times last month that he did not “envision a lot of job cuts” if the firms were split.

EY’s consulting partners have also been separately told they might have their cash pay cut by up to 40 per cent as part of the cost reductions if they split off into a standalone company. This would be offset by the consulting partners receiving shares worth as much as seven to nine times their annual income, estimated to be worth as much as $US8 million.

In short, the split would financially benefit older partners the most, while middle-ranking and junior partners, especially those heading to a newly independent consulting outfit, would face the most risk.

Another detail not mentioned during the briefing is Mr Di Sibio also told the UK paper that the rate of partnership promotions might be reduced to every two years instead of the current annual process. That’s a potential change that would concern any staff member with aspirations of becoming a partner.

However, a spokeswoman for EY said the opposite would be the case, with two independent firms actually looking to “accelerate partnership promotions, possibly promoting more often”.

“We will want to maintain a partnership culture in a corporate model. To unlock growth we will look to accelerate partnership promotions, possibly promoting more often,” she told The Australian Financial Review.

The following slides, which have not been previously detailed publicly, were shown during Mr Di Sibio’s global broadcast, and were part of a wider overview of what was happening at the firm presented to staff late last month.

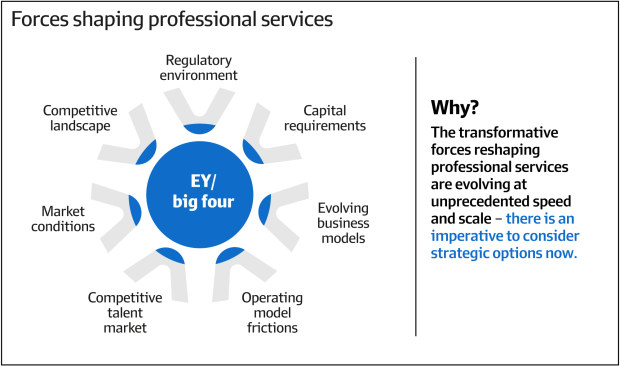

Seven forces ‘shaping’ the profession

One slide outlined the seven forces the firm says are “shaping” the professional services market for EY and its big four rivals, Deloitte, KPMG and PwC.

These include the “regulatory environment”, the “capital requirements” of the firm, the competitive landscape and market conditions.

A note on the slide answering the question of why split stated: “The transformative forces reshaping professional services are evolving at unprecedented speed and scale – there is an imperative to consider strategic options now.”

Not mentioned is that Deloitte, KPMG and PwC have now all publicly ruled out splitting. The senior leaders at Deloitte, who is understood to review potentially splitting on a monthly basis, think that the advantages of having a combined operation outweigh the risks of splitting into two smaller firms.

EY split staff briefing slide.

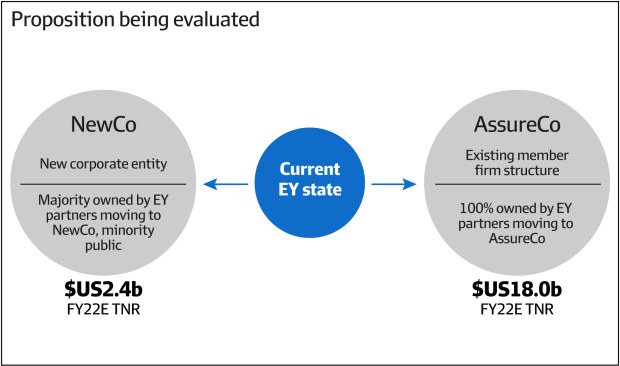

Another slide said if there was a split, the auditing arm, AssureCo, would have estimated revenue of $US18 billion and be 100 per cent owned by partners staying in that business, while the consulting arm, NewCo, would have estimated revenue of $US24 billion and be a new corporate entity majority owned by EY partners moving to the new standalone advisory business.

Not mentioned: how the firm’s existing legal woes would be dealt with. EY’s overseas operations have been at the center of a string of high-profile audit failures.

EY was the auditor of Wirecard, a German payment processor that filed for insolvency in 2020 after admitting that €1.9 billion of cash on its books probably never existed. EY also audited Luckin Coffee, a Chinese coffee chain that filed for bankruptcy filings amid its executives inflated income, costs and expenses.

The firm also audited British hospital group NMC Health, which collapsed amid a suspected multibillion-dollar fraud. The administrators of NMC Health filed a $US2.5 billion lawsuit against EY, alleging negligence in its work on the accounts.

EY split staff briefing slide: NewCo and AssureCo.

A third slide outlined the “benefits and long-term value” of creating a NewCo, boasting the newly independent consulting firm would be “unique in the market” with a “radically different approach that connects design and deliver at every step across advise, transform and operate”.

NewCo would also be able to “expand alliances and strategy partnerships” and raise external capital to invest in “technology, solutions and people” and acquire other firms.

EY split staff briefing slide: NewCo benefits.

A fourth slide reinforced that “any decision must lead to a sum greater than its parts”.

EY split staff briefing slide: 2>1.

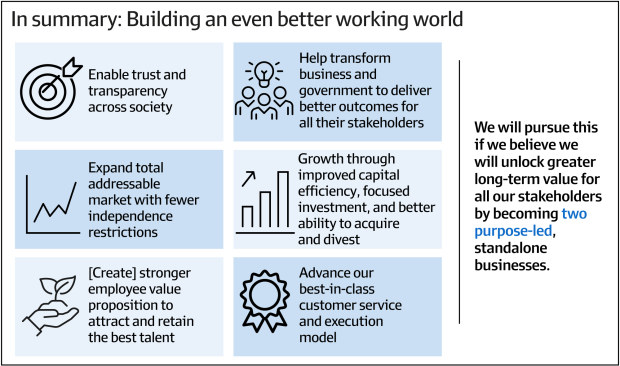

A fifth “summary” slide noted that the firm’s leaders would pursue the split if they “believe [it would] unlock greater long-term value for all our stakeholders by becoming two purpose-led, standalone businesses”.

EY split staff briefing slide: In summary.

A sixth slide outlined what was in a split for employees. This claimed the firm would be “boldly leading professional services” by splitting with the new firms to gain “access to new clients”. It also promises faster growth with more and faster promotions and the ability for staff to “share in the rewards”.

EY split staff briefing slide: What’s in it for you.

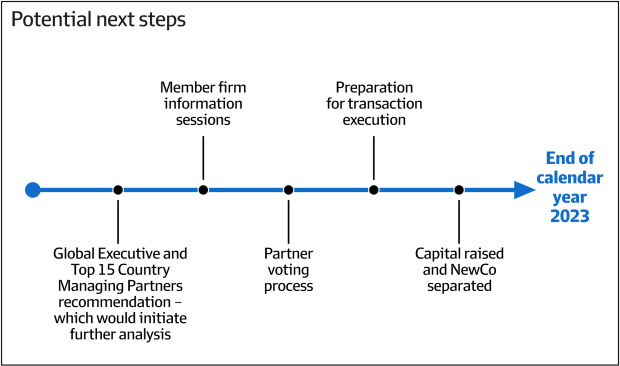

A seventh slide outlined potential next steps for the split. This indicated that even if the 15 country managing partners agree to go ahead with the split, the entire exercise would not be completed until the end of next year.

EY split staff briefing: Timeline.

Mr Sibio has ruled out a trade sale of the firm’s advisory business during the presentation, in part to preserve the culture of consulting division.

This will avoid a repeat of the problems that emerged when EY sold its consulting business to French IT services company Capgemini in 2000. Former leaders at EY and Capgemini have said the sale was a “value destroying” move, with culture shock and an unexpected economic downturn leading to mass job cuts less than two years after the deal.

EY consulting partners should keep in mind the consulting firm BearingPoint. In 2001, KPMG floated its US consulting business as BearingPoint, while the firm’s UK and Dutch consulting businesses were sold to French IT services company Atos for €657 million. By 2009, BearingPoint had filed for Chapter 11 bankruptcy protection.

Mr Di Sibio has cited a range of reasons for pursuing a split of the firm, ranging from increasing regulatory scrutiny of its auditing work, restrictions around the firm winning consulting work from its audit clients and the desire to enter into managed service partnerships with the Silicon Valley companies it audits such as Amazon, Google, Oracle, Salesforce and Workday.

EY’s inability to do partnerships with five of the most important technology companies because it is their auditor is unique to the firm. No other big four audits as many critical technology companies, raising the question of why EY doesn’t stop auditing some of these firms instead of splitting into two.